In a more recent article for Huliq, I outlined the argument in relation to oil:

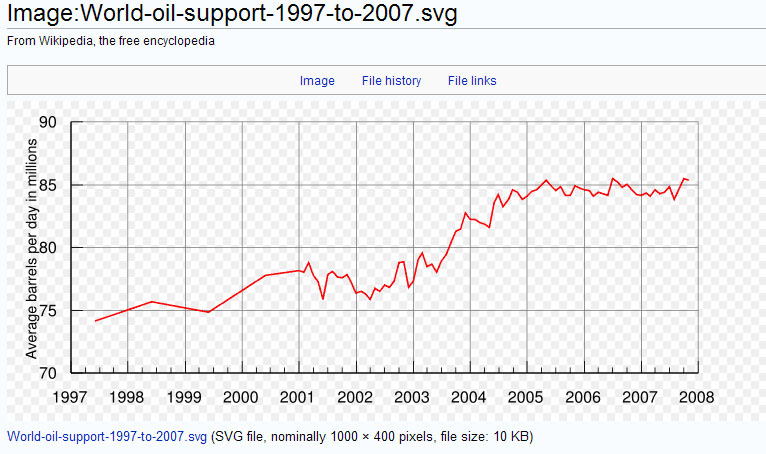

It should be noted here that worker in this context is narrowly defined as labour with access to capital, technology and markets, such that the doubling of the labour supply refers to the full entry of, for example, China and India into the world economy. The result of competition for finite resources means that we have entered what I term a period of 'hyper-competition'.If we take the example of oil, in 1997 output was around 75 million bpd, and output had only climbed to about 85 million bpd in 2007 (a chart here shows the output - not a good source but the chart is usefully clear and conforms to charts from better sources). What we can see from 1997-2007 is an approximate doubling of the labour force, and only a tiny increase in the output of another key component of economic activity.

This quite literally means that the availability of oil per worker has seen a significant decline. In such a situation, there must be a consequence. If a worker in country A increases their utilisation of oil, then a worker in country B will have less oil available.

{kind=link}

The reason why I am returning to this theme is the following news article from the Times:

The desolate, sun-baked deserts of southwestern Bolivia are poised to become the energy battleground of the 21st century, with China and Japan staking early and aggressive claims in the great lithium land-grab.

Japan, observers say, may have won the first round, but, with its mainstream resource ambitions thwarted on the Rio Tinto deal, China could redouble its efforts to gain a foothold in the salt flats of South America and the all-important technology metals.

And also, from the same paper yesterday, we have another related story:

CHINA is stepping up its race to secure access to global oil reserves with an audacious £4.8 billion bid for Addax Petroleum, a London-listed group with fields in Iraqi Kurdistan and Nigeria.

Sinopec, the Chinese state oil group, is understood to have tabled the indicative offer last week, trumping an earlier bid by the Korean National Oil Corporation.

Addax, which has one of only two operational fields in Kurdistan, has seen interest from would-be buyers increase with the completion of an oil-export pipeline from the region.

Sinopec’s approach is further evidence of China’s determination to use its cash reserves to seize control of the raw materials it needs to sustain its rapid economic growth.

What we are now seeing might be described both figuratively and literally as a huge 'land grab'by China. It is figurative in the broad sense that China is using its massive accumulation of wealth to shop for commodities and commodity companies, and literal in the sense that China is now seeking massive deals on the lease of land for agriculture, and is by far the largest player in a new wave of land lease deals (from the Economist):

It is not just Gulf states that are buying up farms. China secured the right to grow palm oil for biofuel on 2.8m hectares of Congo, which would be the world’s largest palm-oil plantation. It is negotiating to grow biofuels on 2m hectares in Zambia, a country where Chinese farms are said to produce a quarter of the eggs sold in the capital, Lusaka. According to one estimate, 1m Chinese farm labourers will be working in Africa this year, a number one African leader called “catastrophic”.

Returning to my recent article in Huliq, it is possible to see that the great game is now afoot, and that game is one in which the most competitive economies will win:

What we are seeing is a competition for the available supply of resources, and it is quite literally a zero sum game [erroneously written as gain in the original]. In such circumstances, the resources will flow to the labour that utilises the resource in the most cost effective way, and where there is the commensurately high return on capital. In other words, where resources are finite, where there is an increase in labour per unit of commodity, then there is a situation of hyper-competition.

The shape of what we are witnessing is slightly different to the way that I envisaged the competion would play out (at least when I first contemplated the way it would play out). My original vision was that it would be the competitive state of economies that would determine where resources would be allocated. Instead of this, the situation is one in which the countries with the greater financial resources are seeking to lock in natural resources through financial fire power.

This approach, in particular the growing activity of China, chimes with two other themes that have emerged in the blog. The first is the ambition of China to replace the $US with the RMB, and the second in the diversification of China's reserves away from $US assets into commodities. In a speculative article on how China might ditch the $US, I wrote the following:

As they move out of $US they would likely buy as many precious metals as possible without driving the price too high, as well as buying into emerging market, European and Japanese bonds. In doing so, they will be taking risks but with the benefit that they will be positioning the RMB as the next reserve currency. Furthermore, it is no secret that China has been trying to buy into various commodity companies (or natural resource companies), such as the ongoing saga of the Chinalco purchase of Rio Tinto or their wider expansion of investments in this sector.

I have been tracking the emergence of the RMB as a world currency over many posts. A strategy of locking more and more resources into Chinese hands would support such a strategy, with potential to influence a move to pricing of commodities in RMB. It is apparent that China is stepping up their determination and will to secure ever more sources of resource.

I have described this as a 'great game', but perhaps game is not the right word. When countries start to compete for resources in this way, one of the outcomes might be climbing tensions between the players. As yet, those tensions are not too heated, but there is worrying potential for this to be the future direction. There are indications that China sees this potential in their development of a 'blue water' navy (e.g. see here), which will allow them to project their power more broadly.

At the heart of the problem is that the massive increase in supply of labour has indeed created a zero sum game. As long as there is potential for shortages of key commodities, the world will remain in a situation of hyper-competition. The worrying part of all of the current activity is that the nature of the competition is perhaps fiercer than I imagined.

Note 1:

I have commented at the end of my recent article on the bond smuggling in Italy. Having rooted around on the subject, I came accross an article on ABC news which reports a massive forgery operation in US bonds, dated February of this year. The forgery includes the large denominations found in the hands of the smugglers. I found the article in a comment (sorry, I forget where), and it appears from the article that the bonds are likely forged. Lemming asks how this squares with the smugglers being Japanese, as the forgery operation is in the Philippines. At this stage, I am not sure.

However, as I emphasised in the article, this was all a little too 'James Bond'. As such, if a rational explanation emerges, I go with that. In this case, there is the underlying idiocy that anyone might have thought that they could pass off such large denominations as genuine. I forget who now, but I think one commentator on the blog pointed to the idea that we should never underestimate stupidity. It seems that idiocy is frighteningly common.....

The alternative is that the bonds are real, and that the forgery in the Philippines is just a coincidence. This coincidence is best measured against the coincidences of the recent Japanese unbridled support for the $US, and the location of the G8 in Italy. From my point of view, the forgery looks more promising....in particular now that it is no longer the North Koreans in the frame (as they would not have been likely to have undertaken such a poorly laid plan).

Note 2: Lord Keynes - thanks for the link to Mises on the fixed money supply. Interesting reading....

Note 3: Lemming - you are right about China, but their industry is currently 'facing' towards supply to the West. As such, any change to domestic consumption will require possibly painful restructuring...