In a more recent article for Huliq, I outlined the argument in relation to oil:

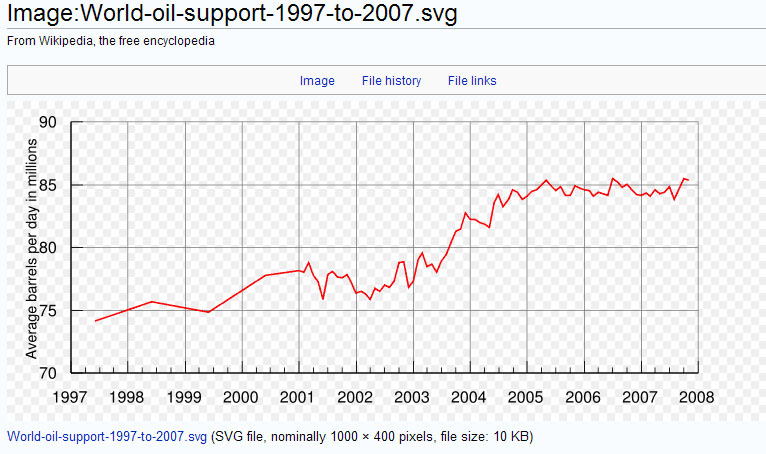

It should be noted here that worker in this context is narrowly defined as labour with access to capital, technology and markets, such that the doubling of the labour supply refers to the full entry of, for example, China and India into the world economy. The result of competition for finite resources means that we have entered what I term a period of 'hyper-competition'.If we take the example of oil, in 1997 output was around 75 million bpd, and output had only climbed to about 85 million bpd in 2007 (a chart here shows the output - not a good source but the chart is usefully clear and conforms to charts from better sources). What we can see from 1997-2007 is an approximate doubling of the labour force, and only a tiny increase in the output of another key component of economic activity.

This quite literally means that the availability of oil per worker has seen a significant decline. In such a situation, there must be a consequence. If a worker in country A increases their utilisation of oil, then a worker in country B will have less oil available.

{kind=link}

The reason why I am returning to this theme is the following news article from the Times:

The desolate, sun-baked deserts of southwestern Bolivia are poised to become the energy battleground of the 21st century, with China and Japan staking early and aggressive claims in the great lithium land-grab.

Japan, observers say, may have won the first round, but, with its mainstream resource ambitions thwarted on the Rio Tinto deal, China could redouble its efforts to gain a foothold in the salt flats of South America and the all-important technology metals.

And also, from the same paper yesterday, we have another related story:

CHINA is stepping up its race to secure access to global oil reserves with an audacious £4.8 billion bid for Addax Petroleum, a London-listed group with fields in Iraqi Kurdistan and Nigeria.

Sinopec, the Chinese state oil group, is understood to have tabled the indicative offer last week, trumping an earlier bid by the Korean National Oil Corporation.

Addax, which has one of only two operational fields in Kurdistan, has seen interest from would-be buyers increase with the completion of an oil-export pipeline from the region.

Sinopec’s approach is further evidence of China’s determination to use its cash reserves to seize control of the raw materials it needs to sustain its rapid economic growth.

What we are now seeing might be described both figuratively and literally as a huge 'land grab'by China. It is figurative in the broad sense that China is using its massive accumulation of wealth to shop for commodities and commodity companies, and literal in the sense that China is now seeking massive deals on the lease of land for agriculture, and is by far the largest player in a new wave of land lease deals (from the Economist):

It is not just Gulf states that are buying up farms. China secured the right to grow palm oil for biofuel on 2.8m hectares of Congo, which would be the world’s largest palm-oil plantation. It is negotiating to grow biofuels on 2m hectares in Zambia, a country where Chinese farms are said to produce a quarter of the eggs sold in the capital, Lusaka. According to one estimate, 1m Chinese farm labourers will be working in Africa this year, a number one African leader called “catastrophic”.

Returning to my recent article in Huliq, it is possible to see that the great game is now afoot, and that game is one in which the most competitive economies will win:

What we are seeing is a competition for the available supply of resources, and it is quite literally a zero sum game [erroneously written as gain in the original]. In such circumstances, the resources will flow to the labour that utilises the resource in the most cost effective way, and where there is the commensurately high return on capital. In other words, where resources are finite, where there is an increase in labour per unit of commodity, then there is a situation of hyper-competition.

The shape of what we are witnessing is slightly different to the way that I envisaged the competion would play out (at least when I first contemplated the way it would play out). My original vision was that it would be the competitive state of economies that would determine where resources would be allocated. Instead of this, the situation is one in which the countries with the greater financial resources are seeking to lock in natural resources through financial fire power.

This approach, in particular the growing activity of China, chimes with two other themes that have emerged in the blog. The first is the ambition of China to replace the $US with the RMB, and the second in the diversification of China's reserves away from $US assets into commodities. In a speculative article on how China might ditch the $US, I wrote the following:

As they move out of $US they would likely buy as many precious metals as possible without driving the price too high, as well as buying into emerging market, European and Japanese bonds. In doing so, they will be taking risks but with the benefit that they will be positioning the RMB as the next reserve currency. Furthermore, it is no secret that China has been trying to buy into various commodity companies (or natural resource companies), such as the ongoing saga of the Chinalco purchase of Rio Tinto or their wider expansion of investments in this sector.

I have been tracking the emergence of the RMB as a world currency over many posts. A strategy of locking more and more resources into Chinese hands would support such a strategy, with potential to influence a move to pricing of commodities in RMB. It is apparent that China is stepping up their determination and will to secure ever more sources of resource.

I have described this as a 'great game', but perhaps game is not the right word. When countries start to compete for resources in this way, one of the outcomes might be climbing tensions between the players. As yet, those tensions are not too heated, but there is worrying potential for this to be the future direction. There are indications that China sees this potential in their development of a 'blue water' navy (e.g. see here), which will allow them to project their power more broadly.

At the heart of the problem is that the massive increase in supply of labour has indeed created a zero sum game. As long as there is potential for shortages of key commodities, the world will remain in a situation of hyper-competition. The worrying part of all of the current activity is that the nature of the competition is perhaps fiercer than I imagined.

Note 1:

I have commented at the end of my recent article on the bond smuggling in Italy. Having rooted around on the subject, I came accross an article on ABC news which reports a massive forgery operation in US bonds, dated February of this year. The forgery includes the large denominations found in the hands of the smugglers. I found the article in a comment (sorry, I forget where), and it appears from the article that the bonds are likely forged. Lemming asks how this squares with the smugglers being Japanese, as the forgery operation is in the Philippines. At this stage, I am not sure.

However, as I emphasised in the article, this was all a little too 'James Bond'. As such, if a rational explanation emerges, I go with that. In this case, there is the underlying idiocy that anyone might have thought that they could pass off such large denominations as genuine. I forget who now, but I think one commentator on the blog pointed to the idea that we should never underestimate stupidity. It seems that idiocy is frighteningly common.....

The alternative is that the bonds are real, and that the forgery in the Philippines is just a coincidence. This coincidence is best measured against the coincidences of the recent Japanese unbridled support for the $US, and the location of the G8 in Italy. From my point of view, the forgery looks more promising....in particular now that it is no longer the North Koreans in the frame (as they would not have been likely to have undertaken such a poorly laid plan).

Note 2: Lord Keynes - thanks for the link to Mises on the fixed money supply. Interesting reading....

Note 3: Lemming - you are right about China, but their industry is currently 'facing' towards supply to the West. As such, any change to domestic consumption will require possibly painful restructuring...

Having just written this post, I have found that treasuries are on the 'up' following a statement of 'confidence' in the $US from the Russian finance minister.

ReplyDeletehttp://www.bloomberg.com/apps/news?pid=20601087&sid=abiCLog4vXgQ

Bearing in mind that Russia was previously discussing a move out of the $US, this is quite a turnaround. Peter Schiff believes that there is a 'pump and dump' going on (link in previous post), but (from the same article as above):

"Investors from outside the U.S. bought $57.5 billion more of the nation’s long-term bonds, notes and stocks than they sold in April, according to a Bloomberg News survey of economists before the Treasury Department issues the figures today. It would be a third straight month of net purchases."

Quite honestly, I am struggling to make sense of it. Do central banks really believe in a US revovery???

The Current Crisis was Predicted by Some Economists

ReplyDeleteIn a relatively obscure journal called the Real-World Economics Review, there is a fascinating piece on how experts on finanical deregulation accurately predicted the current crash:

In October 2008 the British sociologist Laurie Taylor asked listeners of his weekly BBC radio programme to find an economist who had predicted the 2008 credit crunch and financial crisis. The nominations were scrutinised carefully and most were rejected. On 15 October 2008 the radio host announced that the most prescient prophet of the outcome of international financial deregulation since 1980 was the relatively obscure British financial economist Richard S. Dale. In his book on International Banking Deregulation, Dale (1992) had argued that the entry of banks into speculation on securities has precipitated the 1929 crash, and that growing involvement of banks in securities activities resulting from incremental deregulation since 1980 might precipitate another financial collapse ... Hyman Minsky (1919-1996) got some credit too. In a series of papers, Minsky (1982, 1985, 1992) argued that capitalism has an inherent tendency to instability and crisis. The key destabilising mechanism is speculation upon growing debt. Minsky gave a number of warnings about the severe consequences of global financial deregulation after 1980. Although championed by Post Keynesians, Minsky’s ideas were never popular with the mainstream. Yet on 4 February 2008 the New Yorker noted that references to Minsky’s financial-instability hypothesis ‘have become commonplace on financial Web sites and in the reports of Wall Street analysts. Minsky’s hypothesis is well worth revisiting.’

Geoffrey M. Hodgson, “After 1929 economics changed: Will economists wake up in 2009?”

Real-World Economics Review 48 (6 December, 2008): 273-278.

http://www.paecon.net/PAEReview/issue48/whole48.pdf

Mark,

ReplyDeleteRe. "Inflation, Deflation and Money"

A great and insightful post, which I believe brings a lot of clarity to your current understanding of monetary issues. I'm also happy that your thinking on the subject and mine seem to converge. I was composing a lengthy reply, but was overtaken by other, more topical posts from you, about the bond smuggling affair and the current geopolitically themed one, and it seemed pointless to continue with my reply, since nobody would read or comment on it.

It's a pity that we cannot have "twin" threads running on this blog: one dealing with unfolding current events, and another dealing with fundamentals such as monetary theory, trade deficits in general, approaches taken by different economic schools etc. The "theoretical" thread would probably not be as popular as the "current events" one, but from the discussions I have witnessed in the past would probably be very interesting and helpful to many of your readers.

As things stand now, as soon as a new post appears, everybody moves on to it, and the old discussion becomes "dead" for all intents and purposes. Perhaps a simple solution would be to have a "recent comments" tab on your main page, so that people could comment on older posts and be easily "visible" to those still interested in the subject. Just a thought.

Best regards

Matt

ENDOGENOUS THEORY OF MONEY

ReplyDeleteDoes anyone subscribe to the endogenous theory of money?

The view that the money supply is purely exogenous is associated with monetarism, that is to say, that the money supply is determined and controlled by central banks outside of the private sector.

Post-Keynesian monetary theory now accepts that the money supply is partly endogenous, that is to say, partly determined by factors within the private sector

(Rochon 2003).

Steve Keen (the author of DebtWatch) also subscribes to a form of this view.

http://www.debtdeflation.com/blogs/2009/01/31/therovingcavaliersofcredit/

Money supply can, and is, inflated by private banks creating credit and thus new deposits in other banks. Thus increases in money supply can be strongly influenced by the private demand for money:

causation in money creation runs in the opposite direction to that of the money multiplier model: the credit money dog wags the fiat money tail. Both the actual level of money in the system, and the component of it that is created by the government, are controlled by the commercial system itself, and not by the Federal Reserve. Central Banks around the world learnt this lesson the hard way in the 1970s and 1980s when they attempted to control the money supply, following neoclassical economist Milton Friedman’s theory of “monetarism” that blamed inflation on increases in the money supply. Friedman argued that Central Banks should keep the reserve requirement constant, and increase Base Money at about 5% per annum; this would, he asserted cause inflation to fall as people’s expectations adjusted, with only a minor (if any) impact on real economic activity.

Though inflation was ultimately suppressed by a severe recession, the monetarist experiment overall was an abject failure. Central Banks would set targets for the growth in the money supply and miss them completely—the money supply would grow two to three times faster than the targets they set.

All this strongly challenges the Austrian and monetarist theory of inflation and the money supply.

BIBLIOGRAPHY

L.-P. Rochon, 2003, “On Money and Endogenous Money: Post Keynesian and Circulation Theories,” in L.-P. Rochon and S. Rossi (eds), Modern Theories of Money: The Nature and Role of Money in Capitalist Economies, Edward Elgar Publishing. pp. 155-172.

A coupel of fascinating links from a source often cited in Comments here

ReplyDeletehttp://www.globalresearch.ca/index.php?context=va&aid=13969 - by the excellent Michael Hudson who I cited here before on de-dollarization of world trade.

and a shorter article on a similar theme:

http://www.globalresearch.ca/index.php?context=va&aid=13926 - changing world.

@MattInShanghai

ReplyDeleteI have previously suggested a related bulletin board system might be a nice idea. Allowing discussion on old posts, or tangential ideas.

Of course, CE knows how he wants to run his blog and it may be that keeping an eye on a bulletin board is just too much work (they can become really time-consuming) or too far from the original premise of a simple blog.

I enjoyed this latest post. The points (like all of CEs points) seem to get right to the heart of things. Meanwhile, a significant portion of the outside world continues blithely with its fingers in its ears saying : "La la la la, recover has begun."

It strikes me that "The Battle for Resource" may give the Chinese a good reason to keep the value of the USD afloat for as long as they can. Which could delay a collapse in the value of the dollar and resulting steep inflation for a longish time. If they are accumlating not just uncashable IOUs for labour, but also resources with a real economic value, then the sustainability of the US position may not be quite as urgent a priority to the Chinese as you have been suggesting it should.

ReplyDeleteCynicus,

ReplyDeleteFor what it's worth, the rumour on the street in Italy is that the two Japanese work for the Post Office, and had US papers supporting the bonds' authenticity. Of course, rumours are just rumours, but many of the discussions about other fake paper are just rumours, too.

The Japanese Post Office has one of the largest deposit bases in the world.

re: Russia praising the dollar

There were lots of statements about eternal peace and brotherhood right before WWII broke out.

"The more complex societies get and the more complex the networks of interdependence within and beyond community and national borders get, the more people are forced in their own interests to find non-zero-sum solutions. That is, win–win solutions instead of win–lose solutions.... Because we find as our interdependence increases that, on the whole, we do better when other people do better as well — so we have to find ways that we can all win, we have to accommodate each other...." Bill Clinton, Wired interview, December 2000.

ReplyDeleteIs it possible that the difference between this blogs predictions and those you hear on the radio come down to a zero-sum/non zero sum view of trade? What economists view trade as zero sum? The merchantilists and those who propose autarky would seem to.

I find it interesting that you think that the new era of "zero sum" is so significant Mark. It was *inevitable* that this day would come.

ReplyDeleteAre you saying that economists and governments have made no plans or provisions for a state of permanent recession?

This all does sound remarkably like the end of a pyramid scheme, where once expansion is no longer possible, the mechanism collapses catastrophically, with no chance whatsoever of it shrinking gracefully.

Cynicus,

ReplyDeleteThe Huliq article was very helpful in summarising your views - and my own thoughts with regard to them.

I think that you are right in your analysis of an underlying cause for the economic problems: the emergence of more 'workers' (as you define them) in the East has led to a redistriubtion in world capital and a greater Western reliance on debt-based growth.

The 'problem' I have is your seeming reluctance to take the next step and ask why this should be so - these are not facts of life we are dealing with, they are the predictable consequences of certain economic arrangements.

In an age of economic globalism, capital is more or less free to move around the Earth as it pleases - but people aren't. Consequently capital almost always seeks to take advantage of the situation by playing one nation's workforce off against anothers: in this case India and China (where the the democracies are weak and non-existant respectively) against those in the West (and given I describe these as " shamocracies", I don't think I can be accused of a pro-Western bias!). Ultimately, the workers of the East aren't more efficient, nor do they have a stronger intrinsic work ethic - they are simply easier to exploit.

Your 'solution' is for the West to 'become more competitive', but in real terms, this just translates as 'businesses need to exploit people and planet more'; the only way for the West to become as competitive as China on the labour market is to take worker's rights back to, say, those of the early 1900s - which, of course, capital would love to do.

On the other hand, the 'anti-Globalisation' proposes restricting the movement of capital, Tobin taxes, etc.

I think both of these approaches tackle the symptoms of the problem rather than the causes.

I believe we should be looking for solutions in the dissolution of corporate powers through meaningful democratic participation, together with a gradual relaxing of world border controls. In this way we changing the conditions that gave rise to the problems in the first place.

But I'm not saying that this is more likely to happen!

I also think you should bear in mind the effect that technological unemployment has had on the West; we simply don't need people to work as much as they used to.

T.

PS, I like the 'recent comments' link - good idea!

PPS, I'm currently running a high-temperature so my brain aint what it should be - apologies for poor explanations/spellings, etc.

@ Lord Keynes,

ReplyDeleteAt the current stage of my thinking I agree with the neo-Keynsians that the supply of money is mostly endogenous i.e. that the bulk of money "in circulation" is created by borrowers - central banks have only a small degree of influence on the process. CE gave an example of the beer-loving gardener writing IOUs all over town to finance his drinking binge.

The Austrians I think have a completely different perspective, which is that they see a money economy as being fundamentally similar to a barter economy, where goods and services are exchanged for inherently "valuable" commodity-backed money (gold or silver). In this model, the money supply is simply the sum total of all gold (or silver) on the market, and as such does not vary (at least not by much). On the other hand, if one views a money system as being an essentially credit based one, as I do, then the money supply becomes much more dynamic, since money is constantly being created and destroyed.

One can see the why the Austrian viewpoint suits them ideologically -- a barter system does not require the intervention of the state in order to function, whereas a credit system does. I do however believe that the credit explanation of money is far better in describing actual economic reality than the Austrian model.

I'm currently digging my way through the 500 pages of Mises' "Money and Credit", since I've been told that this is the definitive statement of Austrian thinking on the subject. I'll comment more when the occasion arises.

Best Regards

Matt

FWIW

ReplyDelete...."In modern times such fiscal and monetary irresponsibility is unparalleled. This abdication of moral responsibility has already begun the process of dollar deterioration and rising interest rates. The result will soon be hyperinflation.

The collapse may be disastrous for all countries, but it is going to be equally disastrous for the corrupt who have brought us to this sad situation. Hopefully as painful as it will be it could create many new opportunities for some. One thing we see as certain is that the elitists will find themselves targets of civil and criminal charges and targets of contempt and derision. The new world order they so arrogantly and confidentially predicted with one world government will again have been a failure.

There is no question where China is headed in this currency war to dump the dollar...."

https://www.blogger.com/comment.g?blogID=7820485130017459619&postID=7734264316096646535

Some latest articles on the subject of China ascendancy touched in your post:

ReplyDeletehttp://www.atimes.com/atimes/Global_Economy/KF17Dj03.html

http://www.atimes.com/atimes/China_Business/KF16Cb01.html

Interesting take on the latest "green shoots" in the speculative markets:

http://www.atimes.com/atimes/Global_Economy/KF17Dj02.html

And an interesting rant about the WSJ estimate of H. Paulson:

http://www.alternet.org/story/140522/let%27s_get_it_straight%2C_hank_paulsen_is_a_prick_who_took_down_the_economy/

The American Empire Is Bankrupt

ReplyDeletehttp://www.truthdig.com/report/item/20090614_the_american_empire_is_bankrupt/

Hey CE I'm back after a bit of a hiatus.

ReplyDeleteJust checked that ABC story "$2 Trillion in Fake U.S. Bonds Seized"

Now I'm wondering why this google search brings up so few hits.

In fact, the only really relevant hit is the ABC news story.

Try a few variations of the search terms and you'll find almost nothing at all except the ABC news article.

...now if you consider the new close ties between ABC and the Obama adminstration, what do think you have...a state propaganda machine perhaps?

... just sayin'

Re the smuggled bonds:

ReplyDelete"As such, if a rational explanation emerges, I go with that."

I wonder if there ever has been an event that was later found to have been as a result of a conspiracy, even though there was a perfectly rational explanation at the time.

One argument against 'conspiracy' is that there are always too many people 'in on it' and someone is bound to blab. But in the War did the Germans ever suspect that the British were employing hundreds of people to build and operate huge code cracking machines in sheds, and that these people would not mention it to anyone for decades? Hardly a rational explanation for what happened.

The financial system is entirely man-made and the media are not neutral; we see people 'spinning' for advantage all the time - governments especially. Suspecting governments of financial skulduggery is not the same as believing in UFOs.

Further to Lord Keynes' ENDOGENOUS THEORY OF MONEY...

ReplyDeleteDebt-deflation

Web of Debt - THE RETREAT OF THE SHADOW LENDERS: WHY DEFLATION, NOT INFLATION, IS THE ORDER OF THE DAY

http://www.webofdebt.com/articles/quantitative_easing.php

'While contrarians are screaming “hyperinflation!”, the money supply is actually shrinking. This is because most money today comes into existence as bank loans, and lending has shrunk substantially. That means the Fed needs to “monetize” debt just to fill the breach.'

"All of this flap about the Fed driving the economy into hyperinflation because it is creating money on its books reflects a fundamental misconception about how our money and banking system actually works. In monetizing the government’s debt, the Fed is just doing what banks do every day. All money is created by banks on their books, as many authorities have attested. The Fed is just stepping in where the commercial banking system has failed. Except for coins, which are issued by the government and compose only about one ten-thousandth of the money supply (M3), our money today is nothing but bank credit (or debt); and we’re now laboring under a credit freeze, which means banks aren’t creating nearly as many loans as they used to."

"The retreat of the shadow lenders has created a credit freeze globally; and when credit shrinks, the money supply shrinks with it. That means there is insufficient money to buy goods, so workers get laid off and factories get shut down, perpetuating a vicious spiral of economic collapse and depression. To reverse that cycle, credit needs to be restored; and when the banks can’t do it, the Fed needs to step in and start “monetizing” debt.

So why don’t Fed officials just say that is what they are up to and put our minds at ease? Probably because they can’t without exposing the whole banking game. The curtain would be thrown back and we the people would know that our money system is sleight of hand. The banks never had all that money they supposedly lent to us. We’ve been paying interest for something they created out of thin air! Indeed, their credit money is less substantial than air, which at least has some molecules bouncing around in it. Bank credit exists only in cyberspace."

I'm now confused about the hyper-inflationist scenario.

Adam,

ReplyDeleteAnd what happens in say one years time when all debts have been monetised and can be used as a basis for further fractional reserve lending? The answer is Hyper-inflation. How can the treasury reduce the inflated money supply if interest rate rises create further capital reductions and bank insolvency? Monetising debt again will just create an endless cycle of money creation (inflation).

George,

ReplyDeleteDo people want to borrow?

Will banks lend?

I'm taking a time out on the inflationary scenario and considering Mish

The Big Inflationist Scare

http://globaleconomicanalysis.blogspot.com/2009/06/big-inflationist-scare.html