The interesting thing about the analysis is that it is made in the context of the sovereign debt worries about the PIIGS (Portugal, Ireland, Italy, Greece Spain), and the broader worries about the AAA rated larger economies such as the US and UK. His view is that this is a new potentially damaging phase in the crisis. This is how he describes the first two phases:

The first was a fairly conventional, if extreme, banking crisis where a cyclical overexpansion of credit and lending suddenly, and violently, corrects itself in a great outpouring of risk aversion.The reason that this is wrong is that the first phase is not actually the first phase at all. Something else entirely caused the current economic mess, and the risk of sovereign default naturally flows from the real first phase (it is a long post, but if you stick with it, it will be clear why the sovereign debt crises are inevitable). I first discussed the real causes of the economic crisis in a series of posts that steadily built a picture of what was going wrong in the world economy. The posts tracked my evolving thinking on the problem, up to the point where I identified the real cause of the current economic crisis (some of the key posts in the development of the ideas are here, here, here, and here).In the second phase, governments and central banks attempt to counter the economic consequences of this crunch with unprecedented levels of fiscal and monetary support. Temporarily, at least, it seemed to work.

My cause for the crisis does not originate with the financial crisis, but with shifts in the world market for labour. In particular, I track the economic crisis to the massive expansion in the world labour market that commenced with the full entry of China and India into the world economy (as well as a more broad expansion e.g. Vietnam, but these are the two major factors). It might be noted that the labour was already in place in these markets, but the key difference was that there was a change such that these labour markets were connected with world markets, capital and technology. It is impossible to pick a specific date when they started to impact upon the world economy, but I consider the late 90s as an approximate starting point.

If we want to understand the degree of impact of such a change, we just have to think of labour as a factor of production. The greater the supply, the lower the cost of the supply. Both in China and India there are vast pools of labour that is still not fully connected into the labour force, but with potential to be connected. The migration of lower value manufacturing to the West of China is an example of how partially connected labour is continuing to be brought into the world economic system.

What this amounts to is a massive expansion of availability of one of the key factors of production, such that there is an oversupply of labour. However, in order to make this labour productive, it is necessary that the labour has access to the other factors of production, such that the labour might be utilised. These other factors commence with the supply of commodities. I will try to illustrate the point with a simple illustration.

If the world standard of productivity is such that each unit of labour can process 1 unit of commodity, and there are 100 units of labour, the available commodity supply must exceed or equal 100 units for the labour to be fully utilised. If the commodity supply is less than 100, then there will be unemployment/underemployment until the supply of commodities catches up with the supply of labour.

We know that life is not that simple, with variable levels of productivity, but the underlying principle nevertheless applies. In order for labour to be productive, it needs to have a supply of commodity that matches demand according to the potential productivity of the time commensurate with the available supply of the input factor of labour.

What we have seen with the entry of emerging economies is a massive labour supply shock, which is a supply shock that might be regarded as unprecedented in world history (perhaps new world silver supply expansion might be comparable?). The important point about the supply shock is how the supply of the other key input factor responded - the supply of commodities. I will quote from a previous post rather than rewriting the section.

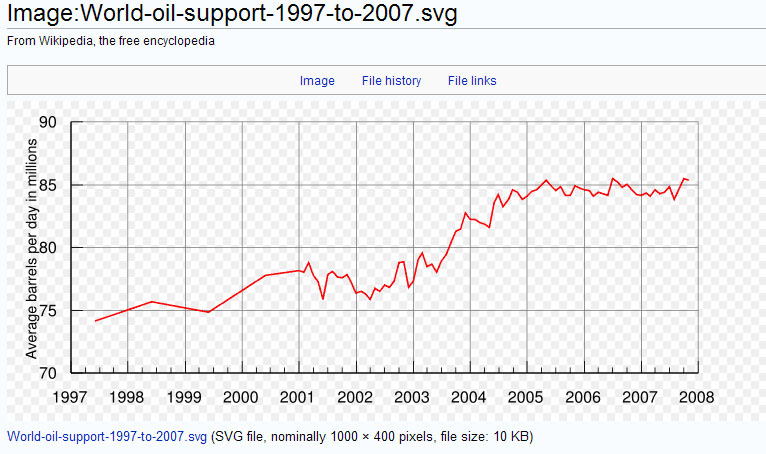

The best example of the problem can be found in oil, as it is still so central to economic activity. In 1997 output was around 75 million bpd, and output had only climbed to about 85 million bpd in 2007 (a chart here shows the output - not a good source but the chart is usefully clear and conforms to charts from better sources). Copper has seen higher growth in output from around 11 million tons to 16 million tons over the same period, but this would still suggest that the growth is still probably not matching growth in labour.The point here is that there has been a major bottle neck in the supply of one of the key inputs to production, and that the supply of other commodities has not fully reflected the extraordinary demands created by emerging economies. The increase in the supply of labour in the world economy was not accompanied by a commensurate increase in supply of materials for labour to process, and for the extraordinary infrastructure development of the emerging economies.

However, not all of the commodities have seen a similar pattern to these examples, with iron ore output nearly doubling over the same period. Whilst this might suggest that there is no problem, it is necessary to remember that countries such as China have been growing infrastructure at an astounding rate, such that their demand for steel will be exceptionally high in comparison with a 'developed' economy (take a look the pictures of Pudong in Shanghai, or Chongqing and you will get a visual sense of one source of demand).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

The other side of this coin is, of course, that the final output of commodities and labour is consumption of the value created by labour in conjunction with commodities. As fast as new labour enters the market, there is a demand for supply of commodities to process, but also increase in demand for consumption of the output of the factors of labour and commodities. Again, a simple illustration will make the point.

If an average Western consumer is consuming one unit of commodities per year, and there are 100 consumers and 100 units of available commodity, it is possible for the one unit of commodity consumption to be sustained. However, if we add 20 consumers per year, and then add only 10 units of commodity per year, it is possible to see that the world average of consumption per person is falling. This, of course, does not make sense. In particular, countries such as China have grown richer, such that the Chinese consumer now has the means to buy more goods and services than before. The point here is that countries like China were so poor, they barely registered per unit as consumers, just as they did not register as labour in the world economy. What is really taking place is a reduction per person of available commodity, alongside a redistribution of this lower per person supply.

In essence, the supply of commodities has increased, but not in a way sufficient for each person to utilise the same amount of commodity as a pre-economic crisis developed world consumer. As such the proportion of available commodities available to places like China is increasing in proportion to the developed world, at the cost of the availability of those commodities in the developed world. The available resources of the world are steadily transferring to countries like China, and the only way for the developed world to maintain the current standards of living is if there is a massive expansion in the supply of commodities.

The big question is how this relates to the sovereign debt crises that are looming. I am afraid this requires more explanation.

If we jump back in time to, for example, the entry of Chinese labour into the world market in relation to the US economy. We see that the Chinese were savers and the US were debtors. It is no secret now that China has been playing a large part in funding the US government deficit and that there have been ongoing negative current account balances in the US. Whilst the US has remained an industrial power house, in aggregate the country has been consuming more than it produces. If we think of the real shift in the balance of resources that has taken place, what we can see is that the Chinese share of the available resources has been increasing, and that it has taken a proportion of that increased resource, and handed it back to the US as credit. This has hidden the real shift in the balance of resource allocation.

In the US, the lending of that proportion of Chinese resource has allowed consumption to continue as if the rebalancing did not take place. In China, it has hidden the real increase in wealth of the Chinese. In the short term, it has appeared that the US is wealthier than it is, and that China is less wealthy than it is. However, the reality is that it is the lending of one country's resource share to another country, and needs to be repaid. If the US does pay, then China will start to increasingly appear as it really is - a far more wealthy country than is presently apparent.

At this stage, you will note that I have not mentioned the financial crisis at all. This despite the fact that nearly every analyst points to the idea that the current crisis was all due to irresponsible lending by the banks. How does this fit into the cause of the crisis that I have discussed here?

There are a multitude of factors that contributed to the crisis, such as the nature of financial regulation, the role of central banks, and the role of government policy more broadly. However, the real root of the financial crisis lay in the provision of ever greater levels of credit to consumers. The source of that credit was from many sources, such as the petro-economies who benefited from rising prices of oil, which in turn reflected the lack of supply matching the increasing demand from the increase in labour. Then there was the supply of credit, exemplified by Chinese lending into the US. Finally, there was central bank policy, best exemplified by the Japanese carry trade, which flooded the rest of the world with Japanese credit, fresh from the Japanese bank's printing press (takes some explanation, see here).

The overall net effect of this was a flood of money into the developed industrial economies. When a bank is offered money, it is highly unlikely to turn it down, and will seek to profit from utilising that money in pursuit of profit for itself and the originator. The problem that arose in this situation of the flood of money is the question of where it might go. If there is a huge supply of money, the first tranche is likely to go into investments in which the risks are well balanced, the second tranche is likely to go into a slightly higher risk investment, and so forth. At any given moment, there are only so many good investment opportunities, and problems arise if there is more available money for investment than good opportunities. However, if there are a dearth of opportunities, then the bank will still find opportunities, even if these are higher risk.

Thus was the consumer boom born, and the service economy built on asset price inflation and debt. This 'new economy' was (in most analysts' minds) different from previous booms, as a virtuous cycle of increasing asset prices supported increased credit, which supported increased service activity and consumption, which increased employment and so forth. The trouble was that, it was not different, but was a massive expansion in credit fuelled by the lending of resource from the rest of the world that needed repayment. The wall of money that was being introduced into the developed world economy was not being invested, but being consumed. If you wanted to invest in productive output, long term investment with a return in wealth generation, all the 'action' was in the emerging economies.

Sure, there were investments in many sectors of the developed world economies, but these investments were largely made in support of the boom in consumption. That consumption was achieved by a combination of internally generated resource, but also with the loaned share of the resource of the overseas creditor. Large sectors of economies were, in the long term, unsustainable.

The financial crisis was simply the unwinding of the many mal-investments as the unsustainable nature of the credit boom became apparent. As the banks made losses, the overseas creditors turned off the taps to the banks. As fast as governments poured money into the financial system, the money flooded out the back door to repay the losses of overseas creditors. If we think about it, as the government bailed out bank A, if the problem was internal creditors, the money would have reappeared in bank B as new credit for lending. Instead, as fast as governments poured in money, it appeared to vanish. The only way that governments could keep the whole system up in the air was to use quantitative easing and massive purchases of distressed assets. In doing so, the losses of the banks, and the losses of overseas creditors appeared on (in the broadest terms) government balance sheets.

Effectively, the overseas credit spigots were turned off, and the only way that credit could be obtained was through the government. The direct credit from overseas lending was simply rechanneled through the government, and thence again appeared in the banking system or as direct spending in the economy. The government had become the debt fuelled consumer of last resort, in an attempt to hide the fact that the economy no longer had the underlying wealth of the past.

If we return to the point about resources in relation to labour, it is very clear that, if the emerging economies were utilising a greater share of a diminishing per person availability of resource, someone somewhere was, by definition, poorer. I was in China in 1997, as a boom in television manufacture took place, along with a boom in the consumption of this good within China. Each television that was consumed in China represented a redistribution of the allocation of the resource of the world into the hands of Chinese consumption, and a move of resource into the hands of Chinese labour. Had the world increased the supply of resources, or commodities, commensurate to the growing supply of labour, this would have presented no problem.

This is not what happened.

We can make an analogy of the resources as a pie. Even as the resource pie is growing, you are confronted with a zero sum game. The number of people sharing the pie is outstripping the growth of the pie, and somebody therefore has to lose. If we want to understand why sovereign defaults are inevitable, we just have to see the actions of governments for what they are. They are pretending that the share of the pie has not moved, and are borrowing the share of pie of others in order to convince their electorates that nothing has changed. The problem is that, even as they borrow a proportion of that pie from others, there is an expectation that it will be returned in the future. Even as the developed world governments borrow, their relative share of the pie continues to diminish, leaving them in a situation where they are committing an ever greater share of a diminishing share of the pie to the creditors.

It is all unsustainable, and no amount of monetary tinkering will change the reality. As labour entered the world economy at a faster pace than resource growth, somebody was going to lose. Monetary tinkering and borrowing will not be able to change this reality, which must somehow emerge.

Note: I have not discussed why the emerging markets have won a greater share of the resources, as the post was already very long. Apologies for this, as it is an important component of the argument, but I am sure there will be many suggestions provided in the comments. There is a great deal more detail that could be added, but I wanted to keep the arguments as simple as I could. I hope that it is clear, and that I have made no significant errors (sometimes it is hard to summarise these kinds of ideas).