I have previously discussed the underlying causes of the current economic crisis, but thought it might be time to update the analysis, and also consider the actions of governments in light of the real underlying reason for the crisis. The focus of the post will be on UK and US, as most readers of the blog come from these countries, but there are many points that might be applied to other countries. As an introduction to the underlying cause of the crisis, I will quote from a post from last year.

The first element to consider is that of the entry of the emerging markets into the world economy. I have dealt with this in the posts 'Why Do Economists Get it so Wrong?' and 'The Root of the Problem'. The argument, at its most basic, is that there has been a massive input of new labour into the world. The labour was always there, but the key difference is that the emergence of these economies has seen capital and technology, and access to markets, become available to this previously underutilised workforce.

The result of this change has seen the available labour force available in the world roughly double in the last 10-20 years. This is nothing short of a revolution in the world economy, but few economists have understood what it really means. This is best expressed in simple terms of an example (using made up figures but referencing the real events) to make the point clear.

If we imagine that (to pick an arbitrary date) in 1990 there were 100 units of labour and 100 units of commodity utilised by that labour, and an available 120 units of commodity capacity (not all utilised), we can see a benign situation. It is a situation in which the commodity supply exceeds demands. We can see this, for example, in the long period in which oil prices were so low for so long. Now, if we jump to 2008, we see the oil prices spiking. This is because, whilst the supply of commodities such as oil has been increasing, they have not been increasing at the same rate as the available supply of labour. Let's call the supply of units of commodity in 2008 a total of 140, to pluck a number out of the air. At the same time we now have 200 units of available labour. At this point, it is apparent that there is a mismatch.

The question arises as to why it is that the problem did not hit at the point where labour first exceeded the supply of commodity. This is because the labour entering the market was not as efficient at utilising the resource as the original labour. It is the catching up, the increase in both the efficiency of the new labour, and the increase in the use of the output of their own labour that has tipped the world into the current situation. (note: I have split the original post into more paragraphs to aid readability)

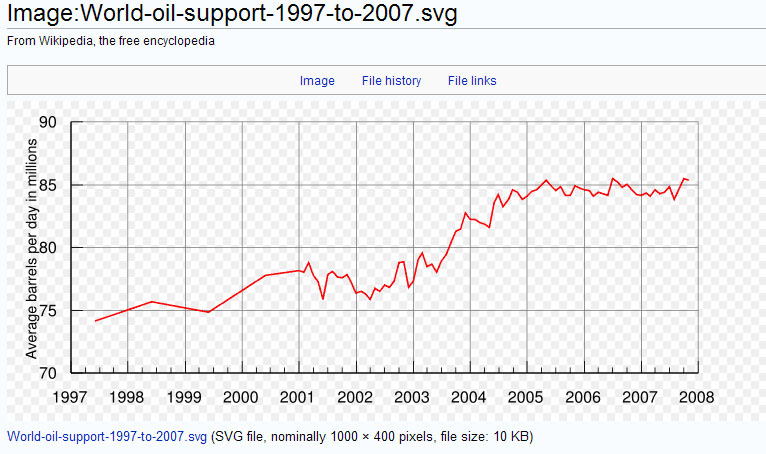

I think it may be helpful to expand on this post, and give some real examples for illustration. The best example of the problem can be found in oil, as it is still so central to economic activity. In 1997 output was around 75 million bpd, and output had only climbed to about 85 million bpd in 2007 (a chart here shows the output - not a good source but the chart is usefully clear and conforms to charts from better sources). Copper has seen higher growth in output from around 11 million tons to 16 million tons over the same period, but this would still suggest that the growth is still probably not matching growth in labour.

However, not all of the commodities have seen a similar pattern to these examples, with iron ore output nearly doubling over the same period. Whilst this might suggest that there is no problem, it is necessary to remember that countries such as China have been growing infrastructure at an astounding rate, such that their demand for steel will be exceptionally high in comparison with a 'developed' economy (take a look the pictures of Pudong in Shanghai, or Chongqing and you will get a visual sense of one source of demand).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

At its most basic, we have a situation in which there are more units of labour, but less units of commodity available to service each unit of labour. In this situation we have a situation of competition for the finite amount of resources, and competition means winners and losers. What we have is a zero sum game in which the utilisation of resource in one place means that it is not available in another place. In such a situation resource will distribute away from the losers towards the winners. However, it is not a winner takes all situation, but rather a competition to see what proportion of the resource is allocated where.

At this point, you may be asking a very reasonable question. You might be asking how, if there is such competition for these resources, the prices of these resources has sunk along with demand for the resources. The answer to this question goes to the very heart of the economic crisis, and why we are witnessing the current economic collapse.

Once again, I will try to summarise a summary of what has happened, before expanding on the ideas. I strongly recommend that you read the original posts (e.g. here), but hope that this summary will serve as an introduction.

The summary of the situation is that the emerging economies lent their new found wealth from their increasingly large workforce into the West, and in doing so allowed the emergence of the so called 'service economy', or 'post-industrial economy'. The lending was built on an unfounded belief that, because the West had been economically dominant for so long, it would always be in a position to pay back the lending. The problem with the lending was that there were no productive wealth creating opportunities to soak up the money, (e.g. investment in manufacturing was being directed towards the emerging economies themselves) such that the money pouring into countries like the UK and US was directed into asset price inflation (real estate), consumption and consumer credit, and excessive government borrowing.

In addition to the emerging economies, we need to add in the flood of money from Japan through the carry trade (I explain this and how the Japanese central bank was responsible for this here). On top of this, the rising demand for oil sent oil prices ever higher, and some of those profits were also recycled into the economies of the UK and US. All of this represents a 'wall of money' pouring into the UK and US that fed the credit and housing bubbles.

All of this lending has had a dramatic and powerful influence on the shape of the world economy. In particular the world economy has been shaped around a perception of growth in wealth in countries like the UK and US, whilst the real growth in wealth has been taking place elsewhere. This takes a little explanation, and starts with the idea of the multiplier effect.

The multiplier effect is where consumption of one 'thing' drives further activity throughout the economy. If we imagine that I spend money in a restaurant, that spending will help do many things, such as pay for the produce, the rent of the building, investment in equipment and pay for staff salaries. If we just look at the payment of salaries, that payment will then be used to pay for other things, and that in turn will pay for the salaries of other staff, who will then use that money to pay for other things and so on....In other words, that single transaction of paying for a meal will result in lots of activity through the economy.

This is all very well, but the problem arises that GDP is widely used as a measure of the success of an economy. The problem is that GDP measures activity in an economy, and this has led to a false perception of growth in the wealth of the US and UK. The reason for this is that activity based upon an increase in borrowing shows up as activity in the same way as any other activity. There is no distinction between sources of the activity. However, borrowing does not represent wealth, but represents the foregoing of future wealth. It is the consumption now of future added value from labour.

A good illustration of how flawed GDP is as a measure of wealth is the example of Hurricane Katrina. This disaster saw the destruction of large amounts of infrastructure, and that destruction necessitated the replacement of infrastructure. That replacement would appear in GDP figures as a growth in activity, and you have a situation in which destruction appears as economic growth. In summary, the huge amount of borrowing in the US and UK appeared as economic growth. There is a perception of growth in wealth in these countries, but the reality is that much of the activity taking place was at the expense of future wealth.

This perception, or I should say illusion, of wealth was to have some dramatic effects on the shape of the world economy. This is best illustrated with some examples.

The first example comes from a conversation with a friend about 2-3 years ago. We were sitting in a restaurant, and I pointed out the large numbers of expensive cars in the car park. There were several BMWs and Mercedes, and other luxury brands, and I asked how it was we could see so many expensive cars. Even ten years before, such cars were relatively rare.

It was actually a rhetorical question, as I was well aware at the time, the reason why they were there was as a direct or indirect result of the credit bubble. If we think of the multiplier effect lifting activity across the economy, we can see that some of the money that paid for the cars was resultant from all of the activity created by borrowed money. As such, when we looked at those cars, they were at least in part the result of borrowed money.

If we then think of the impact of this on the wider world economy, we can see that this will have had a broad effect. For example, this means that there would be investment in additional dealerships to service the demand, and the increase in sales would see additional investment in the manufacturing of companies like Mercedes, and this in turn would encourage investment in the Mercedes suppliers and so forth.

A more mundane example would be the additional money in the pockets of each individual as a result of the borrowed money flowing through the economy. Some of that money for one individual might have been used for home improvement, such as the purchase of new lighting for their house. This lighting that was purchased would likely have been manufactured in the Chinese city of Zhongshan, where there are hundreds of lighting factories. This individual purchase would be one of many that cumulatively saw the investment in ever more factories in Zhongshan to service the overall consumer demand in the UK and US. Each of these factories in turn would have its own suppliers of goods and services, and those suppliers would have their own suppliers and so forth.

Furthermore, the cumulative purchases of lighting would contribute to growth in retail that services home improvements and decoration in the UK and US. This in turn would increase employment in these sectors, which would then have those individuals spending money on other purchases, further raising the activity in the economy.

Such examples illustrate that, as borrowed money flows through the UK and US economy, it shapes the wider world economy to service this credit fuelled activity. The world shapes itself around the consumption. As such, the world economy has been shaped by an illusory perception of growth in wealth.

It is here that we come to the first problem, which is what happens when the illusion vanishes, and when the lending stops. Huge swathes of the world economy are suddenly seen to be pointing in the wrong direction.

I have recently discussed the benefits of deflation, and the effect of this on economic development. However, in the case of the misdirection of resource, there is the potential for a less pleasant (but necessary) form of deflation. This is not deflation resultant from efficiency gains (higher output from each unit of labour), but rather deflation resultant of collapsing markets. As the economy shifts into its new shape, there will be significant overcapacity in industries with a now insufficiently large market.

This overcapacity will lead to fierce price competition before the bankruptcy follows. As such, price deflation should be relatively brief and painful as industries realign to a more sustainable size. In the US and UK, this is being seen in the collapse of the service economy, along with a knock on effect of the suppliers of goods and services into the service economy. If we take the example of retail, they are having to increasingly fight on price, as they chase a diminishing pool of money available for consumption. Some will survive the price competition, others will not. When those that do not survive disappear, there will be a shrinkage in other sectors. A simple example is that demand for shop fitters will fall, such that they will then have to compete on price. These effects will ripple through the wider economy. If we look at our Chinese lighting manufacturers, we will see the same effects.

In all of these cases, what is taking place is destruction of large swathes of economies. This destruction represents the investment of capital, which is in turn the investment of surplus of value of labour. Put another way, this is the destruction of savings. In order to understand this, we only have to think of an empty lighting factory in Zhongshan, with machines standing idle. The idle factory represents the destruction of the accumulated surplus of value of labour. The shops we see with peeling 'closing down sale' posters represent the same phenomenon.

This massive contraction across so many sectors of so many economies is at the heart of the economic crisis. Quite simply, the structure of the world economy was pointing in the wrong direction, and it is now paying the price for that misdirection, which is a massive destruction of capital, which is the destruction of savings.

'What if' the massive wall of lending into the Western economies had never taken place?

I ask this question because it illustrates the severity and depth of the problems that are now becoming apparent. If we think of what would have happened had we not seen the massive lending into the UK and US, and many other credit fuelled economies, we can start to see the shape of the world economy that might emerge.

I will use China as an example of the 'what if' for the big creditors and exporters. In the case that China had not diverted the massive savings into the West, and had used that money internally, then the situation would be very different. The first thing is that the RMB would have risen against the $US, as the ongoing purchase of US debt was one of the reasons for the ongoing strength of the $US. With such a shift, the exports to the US would not have been so large, meaning that the export growth model would have disappeared, and the growth in China would have needed to be more balanced towards internal growth. This is not to say that Chinese exports would not have grown, but the scale of exports would have been smaller.

Alongside this, China would still have steadily accumulated savings which would then have been available for investment within China, which could have seen accelerated growth within the Chinese economy. In all cases, there would have been more money available for consumption within China, and money would have represented a real increase in the living standards of Chinese people. Their savings would have been invested in a sustainable way, and they might have used more of the surplus of value they produced for other things such as health care.

in the 'What if' scenario, what we have is a picture of more balanced and sustainable growth. It would be a model in which China would still have made a major impact on the world economy. It is not possible to drop so much labour into the world market, without a corresponding increase in resource, and for no effects to be felt. Without the amount of resource increasing fast enough, whatever happened, China was going to take a share of the utilisation of resource from the OECD. The big difference would have been that the effect of the shift in resource utilisation would have become visible as it occurred.

What that visibility would have represented for the UK and US would have been a long and painful recession. As manufacturing shifted to China, there would have been rising unemployment, and pressure on real wages to compete with China. This would have been enacted through adjustment of the currency between China and the US and UK. Instead of this process, as fast as the manufacturing jobs were disappearing, they were replaced with the jobs created in the shift to the 'post-industrial' or service economy, paid for out of borrowing. This hid the reality in the shift of real wealth. It allowed the massive misdirection of the world economy into servicing Western consumption.

The reality would have been that Western real wages (in terms of what they could purchase) would have fallen, whilst Chinese real wages would have risen. It would have been a situation where the wages in the two countries would have moved closer together. This is not to say that they would have met in the middle, as the West still had the capacity in industries that could add more value per unit of labour than China, and this would take a long time to change.

This moving together of salary levels would be representative of a more even distribution of wealth, and that distribution of wealth would have had a wider impact on the world economy. At a time when individuals were purchasing SUVs they should have been purchasing small cars. At a time when they were going on expensive overseas holidays, they should have been spending that money at home on domestic holidays. These are generalisations, and discount the variable distribution of wealth, but illustrate a central point. If we take the SUV example, the US car industry expanded production in this area, when the underlying economic drivers were suggesting they should have been investing in small cars. However, this reality was still not visible. They responded to the immediate market signals which were based upon credit driven growth, and are now left with capacity that will never be utilised.

As it is, the what if scenario did not happen, and the result is that the world economy is indeed pointing in the wrong direction, and going through a painful correction as a result. As such it is worth examining what the situation actually is.

The first point is one that I have already explained. Even as I am writing there is a massive ongoing process of destruction. The legacy of that destruction is that there will need to be fresh accumulation of capital, which means savings, in order to transition from the collapsed economic model to a model that better reflects the real distribution of wealth in the world.

In a simplistic example, it might mean that the world market has shifted towards demand for Tata Nano cars, rather than Toyota Corollas. It might mean a smaller market for luxury brands, such as Gucci. It might mean many changes. However, I can not say what those changes might be, as they will be determined both by the redistribution of wealth between countries and within countries. For example, if the Chinese model were to continue as it is, there would be both a relatively large market for luxury cars, a very large market for the Nano, and a medium market for the Corolla. The only certainty is that the shape of markets is changing.

Another certainty is that this move, this transition to the new shape of the world economy, will require significant amounts of capital. This will be needed to rebuild and transition companies to meet the new market demands. The only source of this capital is from savings, and the key to the future is therefore reliant on the accumulation of savings being invested in new productive output to meet the new market demands.

If we look at the big exporting countries like China and Japan, we see that they already have amassed significant capital, and look to be in a position to make the transition rapidly. However, all is not as it seems. In some respects, the growth in wealth in places like China is as illusory as the growth in the wealth of the UK and US was. The way in which countries were accumulating wealth was through lending to countries like the UK and US, and it is here that the illusory nature of their accumulated wealth becomes apparent.

The problem that creditor nations like China and Japan have is that, having exchanged their goods for overseas paper (debt), it is not entirely clear what they can do with such paper. If they sell the paper, they will quite literally destroy the value of the paper, as there is now more and more paper being issued - more than demand can ever soak up. When supply outstrips demand, prices fall, and the addition of sales of any of the existing paper into a market of increasing supply and diminishing demand will simply cause the value to plummet. As such, the paper has little real value, as it can not be exchanged for anything. It is not wealth, but the appearance of wealth.

When the big creditor countries were lending into the UK and US, they were making assumptions that these countries were able to service the debt. The reality that has been exposed in the financial crisis is that there is simply not enough output in these countries to service the debt. It returns to the problem that everybody looked at the GDP growth in the UK and US and thought that this represented growth in wealth.

What we have in reality seen is the consumption within the UK and US of the capital accumulation of overseas countries, with a commensurate rise in GDP as a result. When countries like China and Japan lent money, it was utilised for consumption, and consumption represents the destruction of capital. It is quite literally consumed. The best way to illustrate the consequence of this consumption of the capital of others is through an analogy.

Imagine lending money to a businessman, and later finding that he was spending all of the money on 'parties' and other forms of consumption. You will eventually realise that, without his investing the money in some kind of productive activity, there will come a point where he will be unable to pay it back - he is spending your capital. The US and UK have been having the equivalent of a 'party' using the money borrowed from places like China. As a result, much of the paper held by China has rapidly lost its value. With the borrowed money being utilised for consumption, there has been little investment in output that might repay the lending in value added goods and services.

At its most basic, when a person buys a plasma television made in China using borrowed money, at some point in the future they must repay that purchase with a value of labour with an equivalent value to the plasma television (+the value of the interest). However, instead of investing the money in a way that might help create that value, there has been a move away from development of such investment into investment that utilises labour to service the 'party' (shopping malls, personal trainers, restaurants, entertainment etc.). The shape of the UK and US economies has adapted to facilitate debt fuelled consumption, rather than new wealth creation.

The party is now over, and both sides are looking with regret at this massive consumption of capital. In the case of the creditors to the UK and US, they have seen how their previous lending was spent on the 'party' and are now wary of lending any more to such irresponsible and profligate countries. They no longer want to pay for the 'party'.

More worryingly, in the US and UK, not only has there been a massive consumption of the value of labour of overseas savers, but both economies have also seen a massive contraction in their own savings rates in favour of consumption. As such, both economies are left with a massive hangover of debt, which commits future added value from labour into servicing the debts, meaning that there will be less for accumulation of capital. Both economies have little capital base and the situation exists where both countries must produce enough surplus value to both service debt, and build a new base of capital.

To say the least, it is a very, very painful situation. At the very time when the US and UK need to make huge adaptations in their economic structures, they have nothing with which to undertake the process, and large amounts of what they might produce will go to servicing overseas debt. The US and UK are both entering a more competitive world with nothing left in their armouries. Returning to the 'what if' scenario, this is one of the major differences. If the US and UK had not binged on borrowing, they could have utilised their capital to adjust their economies as the new competitive threat emerged. As it is now, both countries are in no shape to meet the competition.

It is at this point that we come to the actions of both governments, and at this point we should be feeling knots in our stomachs.

The problem confronting the UK and US are the same. In both cases, their economies are transitioning to their real level of wealth. In both cases they are massively in debt, and have very little capital with which to rebuild there economies into the correct shape. Despite this gloomy picture, there is a bright side. Both economies still have large numbers of companies that create significant value, and that value has the potential to start to replace the capital base for each country. Such a process of rebuilding capital would be tough, and would see some very hard years ahead, but would eventually provide a route out of the current crisis.

However, what we see from the government is action which will actively prevent any further formation of new capital, and will see a growing future outflow of money that might have contributed to rebuilding the capital base.

The first problem is that the government is pouring ever more money into insolvent banks in an attempt to move time backwards. I often read that the intention is to save the banking system. However, it is not to save the banking system, but an attempt to save a banking system. In doing so, they are borrowing and foregoing huge amounts of future capital accumulation in order to save an insolvent banking system.

The next problem is that, in borrowing so much money, they are denying the availability of that capital to businesses that might start the process of transition of the economy to the new economic situation. The amount of savings, both domestic and international, available is finite. This means that every $US that is put to use for government borrowing is not available for business. At a time of a massive shortage of capital, governments are taking ever greater slices of what is available.

If we then look at what the governments are using this money for, we can see that (over and above the bank bailouts) they are using it for various 'stimulus' measures that amount to spending. Nobody is hiding that the aim is just to get individuals into employment, any employment, with a view to encouraging them to resume consumption. In all of the government policy, the aim is a resumption of consumption.

If we then think of the underlying problems, we see that this is the worst of all possible outcomes. It is not consumption that is needed but savings, such that there is the capital available for economic restructuring.

If we think back to the idea of the 'party', the governments are trying to tell overseas lenders that when they borrow to encourage the resumption of consumption, it is different to consumers borrowing directly for consumption. They are borrowing to try to make up for the shortfall in consumer borrowing, and trying to restart the party. A perfect example can be found here from the Bank of England:

So it is too early yet for us to assess how far this relaxation in monetary policy is providing support for consumer spending and other elements of private sector demand. (p16)However, whoever is doing the borrowing, it still adds up to yet more consumption, which is the very thing which led to the incredible severity of this crisis.

All the while governments are trying to borrow more to keep the party going, they are also actively discouraging saving. It is well illustrated in the Telegraph, which recently reported on the problems for savers in the UK, with large withdrawals taking place:

As the Bank of England has reduced interest rates to a 300-year low, many savers have seen the return on their money fall to almost nothing. The figures were the latest evidence that savers, who outnumber borrowers by six-to-one, had been cut adrift by the Bank of England, which cut interest rates from 5 per cent in the middle of last year to just 1 per cent in an attempt to stimulate the economy.

The “cash drain”, as the BBA described it, was also a worrying symptom of rising unemployment. People who had lost their jobs were being forced to dip into their savings to pay for everyday expenses.

At the very time that they should be encouraging saving, they are discouraging saving. On top of this, both governments are toying with quantitative easing, otherwise known as printing money. In doing this, they are imagining that they can create new capital. However, all they do is provide a tax on every single unit of currency, as all that happens is that part of the value of the old currency is transferred to the new. This new currency then ends up in the hands of government, who then spend it. Part of that transfer of value will come from savings, further diminishing the availability of capital for investments, and transferring that into government consumption.

At the heart of all the government activity is the failure to recognise the underlying causes for this crisis. All it would take is to direct some of their clever PhD qualified economists to examine the relationship between labour supply and commodities, and the underlying reality of the world would emerge. They would see the reality that we are in a zero sum game, and that reality would translate into an acceptance that wealth has moved away from us. They would then see that the only way that we could return to wealth will be to restructure our economies to meet the new challenges.They would, or surely must see, that this needs capital, and the only source of capital is savings.

Instead, they are continuing on a delusional path, as if nothing has changed in the world. That delusion is driving their every action, and the longer the delusion lasts, the more long and painful the adjustment will be. Their borrowing and money printing adds nothing to the wealth of the countries, but just consumes more capital, and more future capital.

The one certainty in all of this is that the governments can not magic new capital into existence. They can not support the entire economic structure through borrowing, will power and optimism. There is a real world out there, and the only solution is to face up to it.....

Note 1: Regarding the ongoing saga from the Bank of England regarding my questions on the detail of the policy of quantitative easing (QE-Printing money), I have had an email from the BoE requesting a 'chat'. I have asked if they can give me a number to call, and will see what the chat is about.

In the meantime, it seems Edmund Conway has been given further details on the policy of QE, though he does not give his actual source. These are two key passages from his article:

The Bank's governor, Mervyn King, will be granted approval by the Treasury within days to create up to £150bn in new money in the coming months to buy up verything from corporate bonds to government debt. It will pave the way for the Bank's Monetary Policy Committee effectively to "start the presses" at its interest rate setting meeting this Thursday.If you read the article, you will notice that none of it is attributed to any source in the BoE, and it is all therefore unofficial. I am very suspiscious of Edmund Conway who has said the following:

And

But, more significantly, the Bank will indicate in an exchange of letters with the Treasury that it intends to pump a significant amount of cash into the markets, by buying commercial paper and corporate bonds alongside gilts. The amount it is likely to spend on these purchases will probably be around £5bn-£10bn a month.

Those of us who have signed up to the idea that the Bank of England should start printing money have done so on the proviso that that money is pulped as soon as any hints of inflation start to surface.I did not think it was the purpose of commentators and journalists to 'sign up' for policy, but to investigate, analyse and explain policy. What exactly is meant by 'signed up'????

I am genuinely puzzled that these commentators have 'signed up' to this policy. Can they not see the only solution - which is to stop borrowing, cut back on expenditure, and return the UK government to levels of expenditure that can be sustained.

This QE policy will destroy the UK economy, and is no different to what has happened in Zimbabwe. However many clever economists line up in support, the BoE is printing money to pay government expenses, and that is exactly what happened in Zimbabwe. Once started, there is no turning back, and no return to normal policy as suggested by Conway in his articles.

When money is created, it is done through the purchase of an asset. This is done by the BoE simply placing a credit for x amount of money in the account of a broker. In this way money is created. In order to do remove this money, the asset must then be sold, and the credit into the BoE 'disappears' along with the created money.

In the current economic climate, there are very few potentitial buyers of UK bonds out there. We then have to ask who exactly will be buying when the BoE wants to sell the bonds. Their action is to dilute the value of the £GB, and this is more likely to make UK government bonds even less attractive.

Furthermore, look at the ever expanding government borrowing requirements. Who is going to be lending all of this money. The amount of borrowing is growing ever faster...the only way the government will be able to keep up its commitments will be through money printing from the BoE to purchase ever more bonds....are the politicians going to ask for the policy to stop?? And with an election around the corner....

MADNESS. This is sheer madness and the press have 'signed up' for it.

I will keep you updated on progress, and will wait to see if anything official whatsoever comes out of the BoE. However, in the meantime, everything remains very, very opaque despite the article cited above. It all just confirms my belief that the UK government is bankrupt, and is using money printing to attempt to avoid default, and avoid failing to pay for its operations. Very worrying indeed....

Note 2:

I hope the above post makes sense. It is quite long, and I hope that I have not made any silly errors and without an editor, this is always quite possible. If you see an error/problem, feel free to point it out. I will not necessarily change the error, as I follow a principle of never changing a post without a note once it is published (though occasionally cheat on this if I see an error immediately after publication). However, it will help flag this for other readers.

Note 3: As you will notice, this is a long post, so I do not have time to respond to comments on this occasion. Apologies for this.