Some time ago, I was complaining about the increasing opacity/difficulty in obtaining information about the UK economy, for example with the previously wonderful National Statistics now completely hopeless. As such, I have to offer a big word of thanks to Dr. Tim Morgan of Tullett Prebon, who has made an excellent

database of statistics available here, and would also recommend the database to those who are likewise frustrated with finding basic data from the official sites. In practical terms, it means less time looking for information, and more time looking at what the data might mean. This is what Dr. Morgan has to say:

Finding key data on UK issues such as inflation, the economy, spending,

taxation and debt can all too often prove time-consuming and baffling.

The Tullett Prebon UK Economic & Fiscal Database is designed to

contribute to the quality of the public debate by providing all

participants with ready access to objective and consistent data.

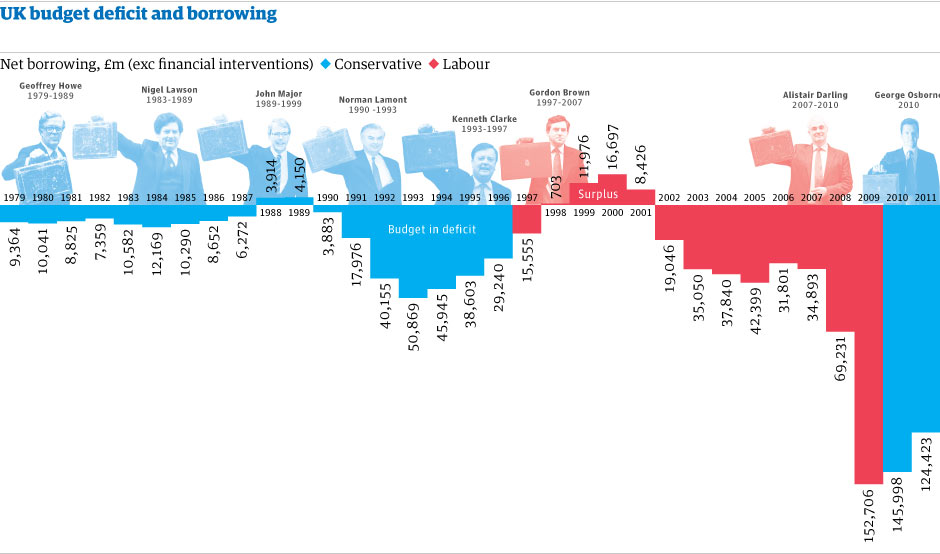

As a celebration of so much easily accessible information, I will today overload on statistics, and use the statistics as a foundation for a review of the UK economy. First of all the government finances, commencing with a breakdown of revenues (billions):

There are a couple of points of note here; the first is that after the drop that took place when the economic crisis became visible, revenue has been steadily increasing with VAT revenue growth particularly pronounced. A commentator recently suggested that the deficit growth was due to a collapse in revenue, but we can see that this only explains a small element of the deficit. With regards to collecting revenues, I

propose a more open, efficient and transparent system, and a system that will also reduce costs and distortions in behaviour. For example, I propose the abolition of all corporation tax, and a flat income tax. Since writing the post on reform, I have identified some problems with the proposal, but still hold with the principles (I may update the post if I have some time).

Below, we have spending (£billions):

I don't think any reader of this blog will be unaware of the growing problems of financing pensions and health with an ageing population. I have often spoken about the necessity of priority; that the government needs to make some hard choices between where an ultimately limited amount of resource might go. I have also argued that there are ways of cutting the expenditure of government whilst also maintaining provision of services and safety nets. For example, as one of the more controversial suggestions, I

propose that welfare becomes an interest free loan with a finite duration and amount. It is a system that would see the welfare share of spending fall, albeit that it would increase government borrowing in the short term. It is a return to the principle of welfare; that it is a safety net. If you look at the links at the top right of the page, you will find solutions to some other areas of spending. I chose the area chart format as they give a good picture of direction of spending and income, but the overview is better represented through a bar chart (billions, at current values):

It does not look very pretty overall. In fact, it look downright ugly. We then have to ask what this is achieving. How is the UK economy really doing? This is unemployment during massive credit expansion:

In this figure, we can see the impact of the boom, and the appearance of the economic crisis is vivid. When looking at the chart, when looking at the fall in unemployment, it needs to be considered in relation to debt, both government (see above) and private:

It is very apparent that debt growth was masking underlying problems in the UK economy. The second chart perhaps is more scary than it should be. We need to remember that the massive increase in aggregate debt took place during a period of high immigration; the massive expansion of borrowing and the activity that it generated had less impact upon unemployment as it also coincided with high immigration levels. This is from the

ONS:

And this reflects in the number in employment:

In these charts, we can see that the rapid credit expansion did dent the unemployment statistics as much as would be expected, as the size of the workforce was also increasing, with significant immigration accompanying the credit boom. The really interesting part is to see what all of these people were actually doing:

Perhaps the most notable point in this, is the increasing size of financial intermediation. Although the figures only go to to 2010, we can see the expansion and subsequent contraction of areas that would be associated with a credit boom; wholesale and retail, real estate. Somewhat surprising is that hotel and restaurants did not see greater expansion. Financial intermediation by contrast, has grown and grown, and (at least as far as these figures go) has not yet started to contract, but I believe that this is now taking place from various news stories (and see below). I took a look at the

2007 SIC codes, to get some sense of what the high expansion in 'all other' means, and examples include legal and accounting, management consultancy, scientific research, R&D, Market Research, rental and leasing of machinery, recruitment consultancy, security services, administrative support services etc. In other words, some of these activities might be associated closely with credit expansion, and other not. Manufacturing is notably flat, as are the primary commodity sectors. Although the chart given above is helpful, it does not give an indication of actual employment, and I dug out some figures from ONS, and created the following (key is given underneath):

A = Agriculture, forestry & fishing, B = Mining and Quarrying, C = Manufacturing, D = Electricity, gas, steam & air conditioning supply, E = Water supply, sewerage etc., F = Construction, G = Wholesale, retail, motor trades, H = Transport and Storage, I = Accommodation and food, J = Information and Communication, K = Financial and Insurance, L = Real Estate, M = Professional and Technical Services, N = Admin and Support Services, O = Public admin, defence and compulsory social security, P = Education, Q = Human Health and social work, R = Arts, entertainment and rec, S = All other services.

The stand outs are the decline in manufacturing employment, Construction, Real Estate, and Retail, albeit that there is something of an uptick in the latter. Also notable is that the numbers working for the state appears to be in decline, but we need to consider this against the increase in 'All other' in the earlier chart of GVA and the increase in Professional Services in this chart; it may be that there is displacement going on here..... Another stand out is the increase in Q, Human Health and Social Work, which now seems to be reversing. A real curiosity is the growth in in D & E, which covers utilities; for E this can be explained by the rejuvenation of infrastructure being undertaken by the water companies (as a guess), but the increase in numbers for electricity is more of a puzzle. As discussed earlier, finance and insurance sees the numbers reducing, which is not apparent in the GVA chart. However, whilst this paints a picture of the post economic crisis, more interesting is to look at what has taken place whilst the world economy restructured in response to the entry of the emerging economies into the system, so I have added December 2000 to the chart, with the label of 'Series 6'. I have placed it next to the 2011 figures to make the changes more apparent.

Manufacturing is startling, even though we have long known this to be the case. For construction, there is still have a way to go before reaching pre-boom numbers, and any reversal of credit growth will mean this sector will shrink even further than pre-boom numbers. If we look at retail now in comparison with unsecured debt now and in 2000 (see earlier chart), the picture is mixed. In contrast to the more recent picture, accommodation and food, however, appears to be an area that may have some contraction if credit growth slows, but there is a question of whether people will forgo retail to continue to enjoy these services, which is a different question, and might mean contraction in retail. In other words, how will disposable income be split between these two sectors if credit expansion stops. Real estate activities still seems to over-large in numbers employed, and still has a way to go down. An offset here is that there are reports of inwards investment into UK real estate, with buyers considering the UK a safe haven. In other words, the sector may yet have 'legs', but my guess is that it is unlikely to last too long.

I have already discussed professional services, and the picture here may be seen as supporting the point about displacement (also see N, Admin support, which may be the same question). However, when looking at export figures, these services appear to have grown, so it is hard to make sense of the figures when aggregated. Education (P) is a real standout for growth in employment. It would be interesting to see how much of this growth is in the tertiary sector, which would reflect the government goals of expanding tertiary education, and also the increase in numbers of overseas students. Whether overseas students will continue to want a UK education is a question that is debatable, as questions are being raised about educational quality (beyond the scope of this post). Finally, we come to another huge standout; health (Q). This stands as an exemplar of the hard choices being confronted by government. In simple terms, each additional person employed in the health system is one less person with potential to be employed in underlying wealth generating activity in the wider economy. And the numbers are going to keep on growing as the population ages. Much more could be said on this subject, but I will leave this open for the moment (at risk of comments that point out that it is not as simple point as I make it).

We now come to wages. Below are some key figures for wages and inflation:

I have titled the chart 'getting poorer', as this is the picture it paints. You need to consider this in light of the ongoing massive borrow and spend of government, and the dubious activity of printing money. Also, you need to consider that the indices for inflation are questionable, and that even if accepting the indices in principle, the impact upon individual households is variable. If we really want to understand something about the underlying nature of the economy, the devil is in the detail (sorry for the messy chart, but it is readable). I have gone a bit further back than the chart above, and this is because of the fascinating story of consumer durables.

You will note how there was significant deflation in the price of consumer durables, which we can safely say reflects the entry of countries like China into the world economy. We can see the peaks in energy prices, and the fall in the same prices as the economic crisis bit home. And now, we see inflation in energy once again; however, this time, the inflation may yet be offset as the global economy teeters (in part driven by higher energy prices), in part by the adoption of fracking. On the other sideof the coin, so called 'green energy' are a potential driver in the UK towards higher electricity prices. The chart below gives annual electricity bills, and it is apparent that they are growing rapidly. It deserves a post in its own right, but there are considerable problems looming for UK electricity supply, and the real cost of 'green' energy is now becoming apparent in Germany (e.g. see

here and

here)

Higher energy prices, it should be remembered, impact more upon those with lower incomes, and the same can be said of food prices. Income spent on energy is not spent elsewhere. The final point of note is that consumer durables have now started to climb in price. If we look at the $US exchange rate, which is the currency of trade, we can see something of the reason (£GB - $US).

Other factors that may also having an impact are rising wages in places like China, and rising energy prices. However, if China does slow significantly, it is quite possible that there will again be deflation in consumer durables; as orders in Chinese factories decline, there may be a period of significant discounting as businesses seek to at least contribute something to their fixed costs. However, the trajectory of the £GB may offset this, and there is ongoing money printing policies in the major economies to muddle any idea of future exchange rates. Competitive devaluation through printing money means that UK money printing effects may be neutralised by other countries printing money. In summary, inflation is very likely to continue, but the degree of future inflation is a very open question. There are simply too many variables that might impact upon inflation in the UK, with UK government and central bank policy simply additional influences.

With regards to house prices, they continue to fall in price in inflation adjusted terms, even if headline prices are relatively stable:

More interesting is the house price to earnings ratio, given below:

By historical standards, they are still high. I must however mention that house prices are, in part, being supported by the inwards investment, as discussed earlier, in particular in London. Nevertheless, the current ratio suggests current prices are not as stable as they may appear. The

Economist also proposes that UK real estate is overvalued compared with rental value (26%) and income (17%), suggesting that real declines will continue at some stage.

My final chart of the day is one I will copy from a previous post, covers the balance of trade, and comes from the (from

ONS):

As I stated in a recent post, it is a good indicator of the long term sustainability of the standard of living within an economy and, again, it is not a very positive picture.

So how can we add up all of these piles of charts? The first point I would like to make is that we can, in part, see that the economic crisis did NOT start in 2008, but started much earlier. It has been so easy for commentators to blame the 'financial crisis', as it evades the fact that there were changes taking place earlier, and that these were simply hidden under the cloak of massive extension of credit. The UK entered the 'financial crisis' already in a state of economic crisis. When looking at relatively benign inflation in the face of credit expansion, the impact of ongoing deflation driven by cheap labour and cost structures in emerging economies was not accounted for. The very real inflation in house prices was ignored; apparently that was un-worrisome inflation. When

I first looked at the UK economy in any depth, it quickly became apparent that the boom years were built upon foundations of credit expansion, and I worried for the future and proposed that people were poorer than they thought. We can now see people becoming poorer in the decline in real standards of living, and the now steady decline in the value of most people's primary asset.

People are becoming poorer in spite of government borrow and spend, which is at astoundingly high levels. When consumers were unable to 'grow' the economy through more debt accumulation, the government tried to 'grow' the economy through debt. Spending tomorrow's income now is not a way to grow an economy, as it will see a shrinkage of disposable income in the future. As it is, private debt is now in a very slight decline. However, this slight decline is more than offset by the massive increase in government borrowing; but incomes still continue to fall. This only serves to illustrate the depth of the economic crisis that confronts the UK. Even whilst borrowing and spending more in aggregate, people were becoming poorer, and unemployment was rising. The UK has not even started to address the crisis that sits metaphorically in front of its nose. It does not take much imagination to see what might happen if the UK was to seriously try to balance its budget. Those £billions of debt generate a large amount of employment. What it does not do is generate underlying wealth; that wealth is generated in the primary commodity industries, manufacturing and the export of services.

These sectors are the ones that are either sitting on plateaus or in decline. Sure, a flood of money into UK real estate might help tide the UK over for a little longer, but that is surely just another repeat of a bubble. There are still such temporary sticking plasters to cover the gaping wound in the UK economy. What these do not do is increase the ability of the UK to export goods and services, which allow the UK to trade in the goods and services necessary to sustain current standards of living. Quite simply, the UK is unable to compete well enough in world markets to sustain the current standard of living. In this post, I looked at government expenditure, and it is apparent that some expenditure is subject to upwards pressure; health care and pensions. These two expenditures look set to rise, even as the UK faces ongoing competitive pressures. In real terms, it means labour being taken from potentially wealth creating industries, and either being redirected into health care, or labour becoming inactive in increasing numbers. The ability to compete with such shifts in the labour force is a challenge the UK must face, in addition to facing the fiercer competition in the world. The UK is not, of course, alone in such challenges, but faces them whilst already struggling to compete.

I keep on discussing this, but it does not do harm to say it again. The so-called 'austerity' of the current government is not austerity, but a luxury; a luxury that cannot be afforded. It is spending borrowed money to avoid confronting the real underlying standard of living in the UK. It is storing up trouble in the face of the challenges of shifts in the labour force, and a less forgiving world economy. So what is to be done?

The answer is to start to question what can, and cannot be afforded. My benefits reform is an example of how a principle might survive intact, whilst seeing reduction in cost. The aim is simple; to allow what was intended as a safety net to return to its original purpose. Real reform, the kind of reform that is increasingly necessary, requires that the shackles of historic legacies be thrown off. The benefits system did not start out as it is now; it evolved over time into what it has become. The same can be said of swathes of policy that comprises the foundation of government expenditure. If you look at the UK's tax code, it is possible to see that the (sometimes) good intentions of government after government has evolved into a sinkhole to drain away productive activity. Instead, the UK has a massive and fundamentally unproductive industry with the sole purpose of managing tax. Can the UK really afford to have so much productive capacity dedicated to what, in the end, is a process of collecting x amount of government revenue?

It is these really fundamental questions that must be asked, and asked of every area of government; what must the government do, how can it do what it must do differently and better, and where are the priorities for what government should do? These are the questions that are still not being addressed. In the meantime, the UK is becoming poorer. I see no change to this in current policy; but rather see the opposite outcome, which is an acceleration of the decline in the standard of living. After all, where is the policy to really address the poor and declining performance of the UK economy?

Note: I hope this is not too 'clunky'; comments welcomed on this and all points of the post. I have covered a lot of ground in this, so please point out any errors you may see.

Note 2: Shortly after publication - I am not sure I have made the best use of the data given - a bit like a kid in a sweetshop gorging without pause. Thoughts / comments welcomed.

{kind=link}

{kind=link}