To start at the beginning, I wrote an article called 'A Funny View of Wealth', in which I identified a fundamental flaw in the UK economy (and which might apply to many other economies such as the US). I wrote it before the financial crisis, and my approach was to review each potentially wealth creating sector of the UK economy. On reviewing each of the sectors, I realised that there was no sector that could possibly explain the apparent increase in wealth in the UK in the 10 years preceding the essay. Instead, what I saw as the only explanation was that there had been a massive growth in personal debt, alongside some growth in government debt (if I recall correctly, I think I included the off balance sheet liabilities). I was very worried, and it turned out, rightly so.

As the banking crisis emerged upon a startled world, I became increasingly horrified at the actions of governments in response to the crisis. I argued strongly that the response to the crisis would eventually backfire on sovereign states, and we are watching this process now unfolding. My analysis of the situation has always been different from every economist, analyst and commentator, and I still hold with my view that the banking crisis was a symptom of an economic crisis, not the cause of an economic crisis. As time has passed, the analyses of the problems have largely been dominated by one, or a combination of, the following:

- It was de-regulation of the banks that caused the problem

- It was greedy short-termism of the markets

- It was the central banks running lax monetary policy

- It was the housing bubble

- It was the credit bubble

- It is an imbalance in world trade

- It is a corrupt stitch up by the banks in conjunction with government

- It is the inevitable result of a fiat money system

I first began to formulate my ideas in a post called the 'Cigarette Lighter Problem'. I asked the question of why an identical lighter, sold through an identical distribution system, might cost nine times more in a Western country than in China. The differential in the cost was fundamentally inexplicable (if you read the article, you will see why). I came to the conclusion that part of the additional cost was actually developed in the accumulation of debt in the economy overall.

As I thought about this problem, I started to think about the cost of labour in the world, and how it was determined. As part of this process the explanation of the economic crisis became clear. In the build up to the crisis, it was possible to see a massive expansion of the global labour supply. Even China by itself represented a massive expansion, but when you add India and the other emerging markets, the labour with access to markets/technology/capital must have at least doubled.

This of itself would not necessarily cause the crisis. As fast as the new labour entered the markets, they might have in turn become consumers, and thereby expanded output for everyone. However, there was a problem. Whilst the labour supply was increasing, the other inputs into wealth creation were not increasing as fast, or were not increasing fast enough to accommodate the massive infrastructure needed to built (from a very, very low starting point) in the emerging economies. If we just think of oil, output barely expanded as the emerging economies emerged, and that means with an increase in the size of the labour force, there was not going to be sufficient oil available for both the West to maintain their standard of living and to see the emerging economies continuing to improve their standard of living. Something was going to have to 'give'. The following is from my article on Huliq, but I suggest that you read the original for the full picture:

I have already identified that the world labour force has roughly doubled in the last ten years. At the same time, there has not been the doubling of the other inputs into the world economy. In crude terms, what this means is that the amount of inputs available to each worker to undertake economic activity has been reduced per capita.For the moment I would like to present a different scenario to what actually took place in response to this problem, and we can see how the economic crisis developed. For the sake of ease I will just use the examples of the US and China to illustrate a general point. If we jump back in time, to about 10-15 years ago, the Chinese economic miracle was in full swing. New factories were pouring goods out of China, and the US consumers were busily expanding their purchase of Chinese goods. As they did so, many US industries were moving offshore, as it became ever more necessary for companies to compete in world markets through lowering their costs. At this point, what should have happened was that there should have been increasing unemployment as the demand for labour fell in the US. With that rise in unemployment, living standards in the US should have started to fall, and at the same time, Chinese living standards should have risen. After all, America was losing in competition to China, and China was winning in competition with America.

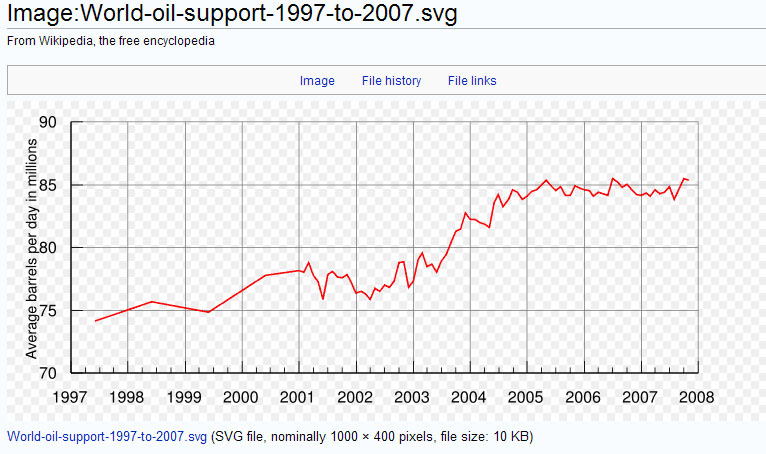

If we take the example of oil, in 1997 output was around 75 million bpd, and output had only climbed to about 85 million bpd in 2007 (a chart here shows the output - not a good source but the chart is usefully clear and conforms to charts from better sources). What we can see from 1997-2007 is an approximate doubling of the labour force, and only a tiny increase in the output of another key component of economic activity.

This quite literally means that the availability of oil per worker has seen a significant decline. In such a situation, there must be a consequence. If a worker in country A increases their utilisation of oil, then a worker in country B will have less oil available.

With regards to other commodities, it might be argued that the output has risen to meet the new demand from the expanded labour force. For example, copper has seen high growth in output from around 11 million tons to 16 million tons, and iron ore output nearly doubled. The problem with such expansion is that it is growth in a period of rapid development of the emerging economies, in which the demands on resources are particularly high. Think of the massive expansion of highways, tower blocks, apartments, airports and factories in China, and it is apparent where such increases might be absorbed.

{kind=link}

As we know, this did not appear to happen. The Chinese appeared to be growing wealthier, but not as wealthy as their prodigious growth might have suggested. This returns to the cigarette lighter problem. If we look at China, the entire economy appears to be low cost. Wages and costs in general are surprisingly low in relation to the increasingly impressive output of goods and services. This is in part because they have still not pulled their entire labour force into the 'modern' economy. It is also partly a result of the value of the RMB, whose value has been held down through the purchase of treasuries. This has meant that, for an ordinary Chinese worker, they are not paid in wages that reflect the true value of their labour. Imported goods are artificially expensive.

What the Chinese have been doing is, as fast as their productive capacity has expanded, and their exports to the US have grown, is lend that missing labour value into the US economy. That missing value turned up in the US economy, and is why the US standard of living did not decline as it should have done in relation to China. All of this gave the illusion that nothing had really changed.

It seemed like China would just get richer, that the US would just get richer, and all was well in the world. However, without an increase in the other key inputs to wealth, the commodities, this could never work in the long run. For example, ten divided by ten equals one, 10 divided by 20 equals a half. If the additional ten lend you their halves, then it can appear that everything is okay, and that you still have one. Of course, in this example, I am being simplistic, as the amount of commodities did increase, but they did not increase fast enough, and China did not lend all of their output. However, I hope that this nevertheless illustrates how the illusion of wealth can be maintained, even as wealth generating capacity is slowly melting away.

What we have is the situation in which a low cost economy is rapidly expanding, endlessly increasing the labour force in the world, consuming more and more resource, and lending a significant portion of their output to another country. At the same time, they are making their already competitive position even stronger. They are adding a further lever to their low cost advantage, and decimating industries and competitors as a result, through holding down the value of their currency. In purchasing US treasuries, they increased the demand for $US, and the increased demand raises the value of the $US, and they also allowed the illusion of wealth in the US to continue through their lending.

However, this is not the whole story. As well as countries such as China lending their value of labour to the US, there are plenty of other actors within this scenario. For example, Japan's export machine kept on chugging onwards, along with the Japanese acquisition of US debt. Then there are the commodity countries, such as the petro-states, or other primary commodity countries. All of these benefited from the increased demand, which itself was a result of the expanding pool of labour. We can think, for example, of a major oil producer in this global picture. In real terms, they are lending oil in the expectation of a return in goods and services. If we go back to the American example, they are literally borrowing oil from the petro-states, and one day they must actually pay for the oil.

Oil is an interesting example of what took place, as it is so central to the functioning of modern economies. We can be buried in the complexities of currency rates, interest rates and so forth. However, when Saudi Arabia lends the US oil, they expect to get something in return.

For example, if the Saudis wanted cheese in return, they might lend their oil based upon the exchange relations for cheese and oil, however abstracted those relations might be. Central to their expectation is that if 1 litre of oil = 1kg of cheese, they will expect that in the future they will be repaid roughly on this rate, with interest added (e.g. repaid 1.3 kgs of cheese per litre of oil). If we look at US cheese output, there may be a nationwide output of 100 units, with 80 units going to the domestic market, and 20 for export. If we imagine that Saudi Arabia starts calling in their oil debt in cheese, we might see the 100 units reapportioned to 30 for export and 70 for domestic use.

What we are seeing is the inflationary impact of debt accumulation. The cost of cheese in the US is going to go up. There is less cheese in relation to domestic demand and, barring a cheese manufacturing productivity miracle, prices must go up. It might be that, with the rise in prices, the US farmer will devote more to dairy, and cheese output will increase, but they would do so by not doing some other kind of farming. The only way to avoid inflation is more farms, or greater productivity from the existing farms, or a combination of both.

Within this simplistic example, we see the principle that issuance of debt eventually creates a call on future output. When is does so, unless there is a productivity miracle, or an increase in the resource devoted to any industry, there will be less output for the domestic market. This means that goods and services will be relatively scarce. For the example of output of cheese, just replace cheese with the total potential output of the economy. You then see the problem with debt accumulation from overseas lending, and why it is inherently inflationary.

Overseas debt is a call on the total output of your economy in the future, and the greater the debt, the greater the proportion of future output needed to service the debt, and the less goods and services available within your economy for domestic use, and the greater the inflation in the economy. Unless there is a productivity miracle, or debt default, then something has to give. There are simply less goods and services available in the economy. Imports can not substitute, as you are already using your output to exchange for past borrowing, meaning you have less output to exchange for imports. As for the example of the US, we can add many other debtor nations to the list of those facing this problem, with similar consequences.

Having explained the danger in the accumulation of debt from overseas, we can start to see the problem. Now, before I go on, there is an important point. Instead of consuming, for example, the oil being lent from Saudi Arabia, lets say that we used this resource for investment in new capacity. Building a new factory, for example, is an energy intensive activity. If we were to use the oil for this purpose, we would actually see a return on that borrowed oil. We have increased our overall capacity to produce goods. Alternatively, imagine an executive used a portion of that oil in a flight overseas to sell a consultancy service. Whilst the oil is consumed, in both cases it is going to generate goods and services that we might sell overseas to repay our overseas loans.

However, this is not what took place, and there is a very good reason for this. The first relates to manufacturing. In the face of low cost competition, investment into manufacturing was shifting rapidly to the emerging economies. In the case of services, the story of India needs no retelling, and again we can see that there was a considerable expansion of competition in many services. However, the money nevertheless was pouring into many Western countries. Where was the money going?

We can only now see the impact of the traditional reasons given for the financial crisis. What we have is a situation where the actual output of goods and services in the economy appear to be increasing. In fact, during a period in which intense competition in goods and services are appearing over the world, there is a strange thing going on. In face of this massive competition, the people in countries like the US appear to be consuming ever more output, even whilst this fierce competition is arising. Not only that, inflation appears muted, and GDP is steadily and apparently rising at a healthy rate.

What we are seeing are two deeply flawed measures. In the case of GDP, it is measuring all of the activity that flows from the resources being lent into the country, in addition to the productive output of the country itself. When we see inflation, it is not capturing the inflation in asset prices. What we have is the miraculous service economy. The money is pouring in from overseas, and that is used to import resources, and these resources are being consumed at an astonishing rate, fuelling profits in companies, and increasing activity around the economy. If we return to the oil example, we can think of Saudi Arabia lending oil to the US, and how that oil might allow for an increase in activity around the economy.

The interesting point about all of the traditional factors for the current crisis is that I would agree that they are all contributory factors in the debacle that we are now witnessing. The one point I would argue with is that it was a result of de-regulation, as I do not accept that there was deregulation, but rather there was misguided regulation. I have emphasised the role of the Basel I and II banking regulation frameworks in contributing to the crisis. There are plenty of easy targets to pick on - for example the Basel II entrenchment of the ratings agencies in the determination of capital adequacy ratios.

As I have long argued, it has been apparent that the regulators have long been of the view that they (and presumably the rating agencies) have some mystical power to see where future risk might be found. Amongst their amazingly prescient determination of future risk, they allocated OECD government debt as being almost completely without risk. Apparently, at this moment in time, banks all over Europe are sitting on piles of absolutely safe Greek government debt, and this debt is a key component in what determined their safe level of capital. The more I dug into Basel I and II, the more silly the provisions seemed.

I even found an article on the Bank of England website that innocently noted that Basel I had been a driver of the market trend to securitisation, the very instruments that later exploded onto the world with the banking crisis. The paper was published pre-crisis, and I wonder if anyone in the central banks would now published, as it is firmly points (with hindsight) an accusatory finger at the role of the regulators. Happily, for the central bankers, the article is now forgotten and gathering dust.

Returning to the question of government bonds being given a zero risk rating, what we see is a regulatory framework that positively encourages banks into buying government debt. A long time ago (I forget which post) I wrote about how, when modern banking was being developed in Renaissance Italy, the city states would grant banking licenses in return for preferential interest rates on their borrowing. What we see now is the same cosy relationship between the central bankers, the banks and the politicians. I scratch your back......

The problem is that, although most people accept government borrowing as if it is some kind of force of nature that is unavoidable, I have yet to see a convincing argument for government borrowing for a developed country, short of war or natural disaster. If governments want to spend more, then just tax more. They have a massive base from which to fund government, so why are they borrowing at all?

Returning to the central point, regulation has played a large part in the lead up to the financial crisis, and has also encouraged states into their current indebtedness. You will note that, as the crisis progressed, central banks and regulators have demanded greater levels of capital to be held by banks - and that is a way of telling banks to hold more government debt - exactly at the time that governments have been increasing debt. The banks are now stacked up with debt which was formerly considered safe, and (in the case of many European banks at present) they are faced with a potential implosion of their balance sheets if there are sovereign defaults.

Are you starting to see the circularity here? However, I have digressed a little from my central theme, which is to set the context of the current parlous state of the world economy.

A key element is the financial services industry. We need to this in the context of a massive shift in the productive output in the world, with inflation in commodity prices. Rather than directly exchanging the profits from these shifts directly into purchase of goods and services, the countries in question have chosen to lend their growing wealth into countries like the US. They do so with great confidence, as they see the OECD countries as more reliable and safe place to lend their money. Alongside this, they see what appears to be healthy and growing economies. What could go wrong?

The problem is that, a wall of money is entering into these debtor economies, and yet there are very limited numbers of investment opportunities, outside of redistribution of the borrowed money into consumption based activity. In particular, if you are investing in the provision of new goods and services for the global market, much of the smart money is going into the emerging economies. So, the banks have a wall of money to lend out, and few opportunities to invest it in places where it might eventually create opportunity for export of goods and services. What to do with the money?

As we now know, the money went into higher and higher risk consumer lending. One result of this was that the money available for lending into mortgages started to outstrip the increase in the number of houses available to soak up the new money. This is, of course, a situation in which more money is chasing a particular good, which means that the price of the good will increase. Thus the housing boom was born. We can see the increase in the money supply into the market with the many highly dubious methods of lending that appeared in the run up to the financial melt-down. What we now see is where the financial crisis comes from.

The bankers were aware that, if you start lending to bad credit risks, then you are eventually going to make some losses. They could hardly sit on the money and do nothing with it, and here we have the incentive for the development of the instruments of mass destruction that were to explode in the financial crisis. The lending was increasingly risky so, within the Basel frameworks, they did everything they could to bury the extent of the risk such that it was out of sight.

The CDOs were rated as investment grade, as per the requirement of the Basel regulations, which had already encouraged securitisation, SIVs, and a host of other practices that were to be seen as precursors to the financial crisis. As a result, it seemed that the banks were making miraculous profits, bankers achieved their amazing bonuses, all at the same time as they were loading up on thinly disguised and regulator approved risk. Remember, the regulators and ratings agencies apparently had a privileged and magical insight into where risk will occur in the future.

We then move onto the role of the central banks, and their contributory role in the mess that we are all now in. Their role was one of astounding stupidity. They were the people paying attention to their metrics of GDP and inflation, all the time having absolutely no idea of what these actually measure. All they could see was the mass of activity in the economy, and did not realise that a large portion of that activity was simply the use of resources borrowed from other countries to move around and distribute borrowed resources lent by other countries. They imagined that all of the activity was from internal resources generated by their own countries output. The really mad part was that, the more that was borrowed from overseas, the greater the activity in redistribution, and the more they believed that the country was getting wealthier.

As a result, with low inflation, and steady GDP growth, they kept interest rates low, and poured more fuel onto the fire with expansionary monetary policy. All this despite asset prices going up at a rate that was disproportionate to the actual underlying state of the economy....

And then there is government. Like the central banks, they were equally as deluded by their use of inflation and GDP figures. Perhaps the worst example is Gordon Brown in the UK, who absolutely convinced himself and nearly everyone else that an economic miracle was taking place. Everyone was becoming richer. In these same countries with the miraculous service economies, governments started letting go of any sense of fiscal caution, in the belief that the good times would not end. They expanded or started new government programs, benefits and entitlements, creating ever more structural government costs, on the basis that their economies seemed to be endlessly expanding. In reality, it was only indebtedness that was expanding, as their economies were in reality stagnant or perhaps even contracting in some cases.

What we were seeing was an illusion of success in many economies, and all the while they were sowing the seeds of future destruction. The increase in debt in economies like the UK and US was simply hiding the structural change that had taken place in the world economy, the emergence of the emerging markets, and the competition for a finite amount of resources amongst an ever increasing labour force. The illusion of the service economy was simply the distribution and consumption of the borrowed output of labour of overseas countries. Houses became ATMs, new shopping malls were built, and new services were developed to consume all of this apparent wealth.

The financial crisis was the shock to break the illusion; or rather it should have been the shock to break the illusion. The madness of consuming future output now was laid bare. However, rather than break the illusion, the choice of governments and central banks was to try, as hard as they could, to continue the illusion.

In the period since the financial crisis, there has been no action to address or recognise the problem. Instead, the reaction has been a host of measures to try to restore a situation that was, of itself, a delusion.

Front and centre were the bank bailouts. The process was not only one in which government money was poured into the banking system, but also a process of allowing the banks to hide their underlying insolvency. Governments have also borrowed to support the existing economic structure, which is an attempt to maintain employment and activity, which is itself an attempt to support (for example) real estate prices, which in turn supports the value of bank assets, which in turn supports the viability of the financial system. It is all circular, with one element supporting the other, with overseas borrowing the foundation of the system. It is impossible to tease apart the circular relationships. Governments must keep on borrowing more and more, or the whole edifice falls apart.

Effectively, when consumers stopped borrowing, government stepped in to fill the vacuum. The problem is that, in doing so, they are supporting the unsupportable. I have previously laid out the contradictory nature of this process in my last post. We have a process as follows:

- A government borrows money from overseas

- The money is spent by the government and this increases activity in the economy

- Individuals who would otherwise be unemployed are able to buy houses, pay back loans, service mortgages, buy goods and services

- Individuals and businesses pay more taxes

- Government revenues are supported

- GDP is supported by all of the activity, either preventing a dramatic fall or slowing of GDP growth

- The relatively good health of the economy reassures investors (e.g. some investors actually believe that the US is recovering)

- Investors are willing to extend further credit

The other result of borrowing more is that more borrowed money supports the level of GDP, which means that the more a government borrows, the higher the GDP. All the borrowed money supports activity within the economy, and this gives the appearance of a healthy economy. This allows for a better debt to GDP ratio, which is, of course circular.

For example, if a government were to double their overseas borrowing overnight, then they would be able to massively increase activity in the economy. GDP would climb rapidly, and the result would be that the GDP to debt ratio would look much better. What you have done is pulled a massive amount of future activity into the present, and this would flatter the size of the economy. However, the GDP outcome does not represent your own generation of activity, but consumption of the output of others, at a cost of committing your own future output. In other words at the cost of a future shrinkage in your own activity. Unless you just keep borrowing more and more.

And here is the problem. Unless you keep borrowing more and more, there is no way to sustain your GDP level, and no way to keep the GDP to debt ratio looking positive. As soon as you stop borrowing from overseas, you are then in a position of repaying the debt that you have already accumulated, and also doing this when your economy is fragile. It is fragile because the structure of the economy has still not managed the adjustment to the new competition from the emerging economies. Government has borrowed to consume to support the structure of an economy that was already built on excessive borrowing from overseas. There is still a period of adjustment to the real structure of the world economy to take place. This can only be achieved through seeing the destruction of the swathes of the economy that were supported through the distribution and consumption of resources that were generated from overseas.

This returns me to the example of the US economy, in which I showed that 17% of US GDP may be accounted for by activity in the distribution and consumption of resources borrowed from overseas. As yet, nobody has contested this figure, though it is certainly open to challenge (see here for the original post). Even if I am roughly right, we can see what happens if the growth in debt halts. We would see a massive contraction in the US economy, and the debt to GDP ratio would deteriorate in a shocking way. It is similar to what we are seeing in Greece. Businesses will close, unemployment will explode, government revenues will fall, asset prices will fall, banks will go bust, and the economy will fall off the edge of a cliff. As this happens, it will become increasingly impossible for governments, businesses and individuals to service the debts that have been accumulated as part of an economic structure built on foundations of sand.

The really horrific part of this is that it is not just the US that is in this terrible position. This is a widespread problem. Furthermore, the structures that have been built to protect failing sovereign states is built upon credit coming from many of the states that are now at risk. One interesting development is that the US is now questioning their role in the IMF bailout of Greece, and is recognising that the credit it would supply would fall into a black hole, and that it can no longer afford to bail out other countries. After all, the US finances are themselves flashing red warning lights. I pointed out in a previous post that, in reality, although the US appears to be a major funder of the IMF, it is in reality the creditors to the US that are really funding the IMF. If the US were not able to borrow more money, would they be able to finance the IMF as they have traditionally done in the past?

Where is the money for IMF bailouts going to come from in the future? It is a question I asked at the start of writing this blog, and it only now that it is apparent to the world that there is a problem. When both the 'bailees' and 'bailouters' are broke, what happens then?

In Europe, it is possible to see the increasing queasiness at having to bail out their fellow European states. The fact that the bailing out of another state means borrowing more, and taking the sovereign debt risk of other countries onto already stretched balance sheets, means that the bailouts can only go so far. The problems do not stop there. For example, if Greece defaults on its debt, this will impact Germany through, for example, their banking sector's exposure to Greek debt. If Greece falls, it may take elements of the German financial system with it. Such is the complexity of the edifice of debt that has been created around the world, and the complexity in the linkages in the destiny of sovereign states.

Niall Ferguson famously coined the phrase Chimerica to express the interdependent relationship between China and the US. The US used Chinese credit to purchase Chinese goods, and then plays a major role in the support of China's export sector. The two countries are inextricably tied in dysfunctional relationship. If either side blinks, they both plunge. However, the contradictions of a developing country (China is still relatively poor) supporting the rich lifestyle of the US must be a finite arrangement. Both sides need to extricate themselves from the relationship, but neither side seems to know how.

In recent news, China has recommenced the purchase of US treasuries, and Chimerica is once again in full swing. This means that, for the moment, the US might continue to finance their dizzying deficits. I think that we are safe in assuming that China is restarting the relationship because they can no longer see any clear alternative. However, as they have hinted at in various statements, China knows that Chimerica is unsustainable, and the US appears to realise this too. In both cases, it is possible to sense that they both hope that something will turn up. In the meantime, the scale of the problems for the future grows and grows.

The only way to describe the trading relationships across the world is 'dysfunctional'. They are relationships built upon a foundation as follows: country 'x' provides country 'y' with credit, and country 'y' uses that credit to buy goods and services from country 'x' and country 'z'. Country 'x' builds an export market in country 'y', and therefore needs country 'y' to keep buying their goods, in order for them to maintain employment and growth. Japan needs the US, Germany needs Spain, China needs the US and so forth. The recipient countries must keep buying, but increasingly have less and less capability to repay the money they are borrowing. The country 'x's reach a point where they are confronted with the reality that they are, in effect, almost giving their goods and services away, as they will never be paid for them. However, if they stop, their own industries will collapse, as they are structured towards servicing these debtor markets.

When German workers wince at the Greek bailout, this is the logical conclusion of the dysfunctional relationship. German credit has allowed German exports to Greece (of course, this is not a one to one relationship, but I use this case for simplifying some complexity). If Greece defaults on their debt, German creditors will take a haircut. If Greece is bailed out, the German government will, through the tax system, make the German worker pay for the Greek bailout. In either case, Germany will have, in real terms, been providing goods and services to Greece at massively subsidised cost, or in extreme circumstance free of charge. In all cases excepting full repayment of debt from Greece, Greek consumption is being subsidised through the labour and efforts of overseas workers. It does not matter which of these many creditor/debtor nations we can look at, the relationship is basically the same.

In each case, in each of these relationships, the dysfunctional accumulation of debt continues, and always with the hope that 'something will turn up', that the debtor nation will miraculously turn around, and start earning more than they consume.

However, the debtor nations have become credit addicts, and become ever more dependent upon the credit to sustain the structure of their economy, which is itself structured around debt. The more credit they get, the more their economic structure will be shaped to utilise the credit. The population of each country is unaware of the source of their apparent wealth, which is too abstract to understand, and they then resist any reform which might mean that they have to accept their real level of wealth. The politicians cave in, and hope that something will indeed turn up (or that they are lucky enough to be out of office when the contradictions of the situation are forced to resolution).

In the end, the creditor nations must blink. They will only support the profligate so far. Like the debtor nations, the people of the creditor countries are unaware that they are in effect, giving away a portion, or all of their labour, to other nations. When it becomes apparent, as with Greece and Germany, that this is the reality of the situation, they are understandably resentful. However, they do not realise that, if the situation halts, then many workers will find that their particular industry, their individual job, is pointing at a market that was entirely reliant on the credit that they have been providing. When their own country turns off the credit taps, the markets for their goods and services will evaporate. They have been pointing their industry and labour to the wrong markets, to markets that were never really going to pay for their goods and services, because they do not have enough output that they are willing to return.

In practice, what happens is that all the savings of individual workers are exposed to the losses that will follow the non-payment of debt. When a person invests in a pension fund, puts their savings in a bank, they are deferring their own consumption. In principle, their money should be channelled into new investments which will produce a future return. Instead, through whichever conduit, their savings have been used to support consumption in the debtor nations. If Greece defaults on debt, and German banks take a hit, this is not abstract money, but the accumulated savings of individuals aggregated and lent into the Greek economy.

I hasten to add that, as they currently operate, the markets are not all relatively ‘benign’ movements of savings and investments. The infamous speculators do exist. However, I have no problem with these people risking their money, for example betting against the Euro. What I do object to is naked credit default swaps, and any of the many other practices that border on the fraudulent, or the way that government backstops the risk, or the way in which governments have entrenched and supported an elite of bankers.

Returning to the central point, the deferred consumption of German workers has instead been consumed by Greek workers, and they are not going to return that consumption with goods or services for the German workers to consume. The deferred consumption has been forever consumed.

The point that I am trying to make here is that this is not as abstract a situation as many analysts and commentators try to make it. It is about the basics of person 'A' manufacturing good 'B' or providing service 'C' to person 'D'. This is the core of economics. It is not mountains of abstract data, but about how this process works in practice. At the heart of the system is that the savings of person 'A', their deferred consumption, is aggregated and offered to others in the belief that it will be returned one day in goods and services for their own consumption.

The expectation of each worker who defers their consumption is that, at least, their savings will be returned in an a way that gives them access to an equivalent amount of goods and services to those they might have consumed at the time of the investment. This is a reasonable expectation, and is the source of potential for sustainable economic growth.

The problem arises when the systems for the allocation of those aggregated savings go wrong. This is the dysfunctional trading relationships between countries. Those in government, in the financial services industry, the analysts and economists, all misunderstood what they saw. They made false assumptions as follows:

- Just because a country has always been wealthy, it will always be wealthy

- Just because a country has a good credit record, any amount of credit might be given to that country

- GDP = Wealth creation

- Inflation measures are meaningful, even when asset prices are inflating outside of the recorded figures

- Trade imbalances might be eternally sustainable where the cause of the imbalance is in consumption activity of one actor of the goods and services of another actor

These assumptions were built upon a world that no longer existed. The entry of the emerging markets, and the newly intensified competition for a finite amount of resource changed the game and the structure of the world economy. As the emerging markets emerged, we entered a period of hyper-competition.

Instead of confronting the competition, much of the developed world simply borrowed and pretended that nothing had changed. The assumption was that the rich world would get richer, and the developing world would get richer. It never occurred to any of the economists, politicians, analysts, and financiers, that with finite increases in resources, we had entered a situation similar, albeit not the same as, a zero sum game. While the pie of resources was getting larger, the number of actors eating the pie was increasing faster still. Just because some of them were lending some of their share of the pie, did not alter the problem that the share of the pie was changing.

So it is that we come to the situation today, with a world economy in which false dawns, endings of the 'financial' crisis, come and go. New solutions are tried, more illusionary gains are achieved, only to see the underlying and unaddressed problems bubble back to the surface. We can see that, despite the efforts of government, many of the rich world countries are indeed getting poorer. The austerity program proposed in the UK may just be an example of this process in action, and we can only hope that austerity can resolve the problems gradually. However, the actions of having tried to prevent change make a gradual rebalancing the least likely outcome, though not impossible.

It is never pleasant to be relentlessly gloomy. I have offered consistent pessimism. I do so because, I believe, I have identified the underlying causes of the economic crisis. In doing so, I believe that the actions to try to turn back the clock are wrong. The only way to move forwards is to resolve the imbalances, and take the pain sooner than later. In accruing ever more debt, in seeking to prop up systems that can not be supported, it may delay the pain, but at a greater cost later. At each stage of the economic crisis, I have repeated the same message.

The only way to resolve the crisis is in the structural reform of economies, and to face the fact that, with a finite pie, and more actors seeking a share of the pie, the only solution is to win the greatest share of the pie possible through efficient development of industry and innovation, and having lean and effective economies. This means that we must trim the fat from our economies. We simply do not have the resource to maintain the lifestyles to which we have become accustomed.

We also have to face up to the imbalances in the world economy, and accept that these are finally unsupportable. Country ‘x’ can not and will not provide goods and services to country ‘y’ at subsidised rates forever. In particular, now that the inability to repay is being highlighted, the real choices for the creditor nations are becoming clear. The reality of the imbalances is now showing the underlying choice – continuation of giving something and getting very little in return, or a painful period of restructuring of their own economies to reflect the real distribution of wealth creation and resource.

I also accept that, in this hyper-competitive world, we are unlikely to win as great share of the pie as before. In an ideal world, the resource pie might expand infinitely, but this is an unlikely outcome at our current position in history (a debate I will leave aside for the moment), and we might have to accept a period of hyper-competition for a long while. After all, there is plenty of labour out there that is still yet to be connected with technology, capital and markets.

It is not an easy message to digest. However, if we wish to address a problem, we have to face up to the actual causes of the problem. As long as the policymakers seek to ignore the real problem, we will continue down the wrong path. It does seem that, with the emergence of the problems of Greece, there are the first signs of accepting that the situation can not continue as it has done. Greece is a warning, and we are collectively starting to take heed. Whether this translates into effective action, and above all acceptance of the reality of the situation, is still uncertain. I can only hope that it does, and that it is not too late.

Within this perspective on the world economy is a further worry. I blithely suggest that we need to adjust, but I also identify that the people of the creditor and debtor nations have not, and probably will not, fully grasp how this mess arose. We see this in the riots in Greece, and the growing anger at the politicians in Germany. The adjustment is going to be very, very painful, and this presents significant dangers. In order for the adjustments to be made, both debtor and creditor countries will suffer painful adjustments. The whole world economy will go through a painful adjustment. In such circumstances, with unemployment growing, and complex and difficult to explain causations, it is a period in which social and political instability will rise.

It is a time in which some people will offer easy solutions, will blame group ‘x’ or group ‘y’ for all of the ills, who will grab the popular anger, and will use that anger for their own ends.

The situation I have outlined in this post, the causes of the economic crisis, are not down to any individual country, or any single group. The bankers were greedy, the regulators were idiots, the Chinese were mercantilist, the Western politicians acquiesced to the Chinese mercantilism, when the politicians promised something for nothing, the press acceded, and the people with them. I could go on. In the end, we all played a role in building this mess.

In addition, the situation is not one in which there will be any painless fixes. We have collectively spent years building an illusionary economic structure. As that structure adjusts, and it must adjust, there is no way to do so without pain for everyone. How we might deal with the adjustment is a matter of debate, but there is no way in which it can be done without pain being felt by ordinary people. However, there will be those who will offer ‘clever’ solutions. They will ‘magic’ away the problems. How this might take place, when the problem is the structure of the world economy, is a mystery. However, they will dress up their magic with plausible and complex argumentation, and in the end avoid accepting that there must be some kind of pain.

In the scenario I have painted, it is apparent that there must be pain that comes with the restructuring. I do not hide this. For governments, the key is not to try to halt the restructuring, but to seek to ameliorate the worst of the effects. It is a fine balance between restructuring and, in the case of the ‘rich world’ getting poorer, and maintaining social cohesion. The danger lies in the pretence that no restructuring is necessary, and that pain might be avoided. The danger lies in governments squandering their resources, as they already have done, in propping up a system that is inherently unsustainable and inherently unstable.

In a very long essay, I have suggested a system that might prevent these problems happening again (it can not ‘fix’ the current problems, but might accelerate their resolution). It is not a perfect solution. No system, for example, might have fully absorbed the labour supply shock that the world has seen. However, the system I have proposed would have prevented the imbalances that followed the supply shock. It is a system which is largely self-regulating, bubble resistant, and imbalance resistant. However, I suspect that such a system is only a dream, as it removes power from those who would like to hold on to their power. I therefore offer it as a solution, but also as a solution that is unlikely to be adopted.

Note 1: When first posting this solution, my use of the concept of value of labour led one commentator to suggest that it was Marxist. The concept of value of labour used is very different from that of Marx, and the solution is in no way Marxist. Also, a regular critical commentator on the blog, commenting under the name ‘Lord Keynes’ has recently said the following:

“Cynicus’ variant on the labour theory of value, in which he believes that value is both caused by subjective factors and by labour is logically inconsistent.Value cannot be subjective and also caused by labour.”It is entirely consistent to say that we subjectively value labour, which is my explicit central point. I see no inconsistency in this. Lord Keynes simply misrepresented my argument to create an inconsistency. From this commentator, there will no doubt be essays in response to this reply. I would therefore ask you to read the original.

Note 2: As ever, please feel free to comment on any aspect of the post. Even in a post as long as this, in order to cover breadth I have had to sacrifice depth. If any point is unclear, I have expansions on each of the points littered throughout the blog. Also, in trying to compress many arguments, I hope that the arguments are not weakened or might appear inconsistent. Finally, there is the sin of ommission. For example, I do not include the many additional mercantilist Chinese practices that I have included elsewhere in the blog, or the dangers in quantitative easing (printing money), or many other key points. In short, an overview can only be an overview.

Note 3: Thanks for the interesting comments on the last post. I recently found that I had missed following one of your links on a previous post, which was to a You Tube video of the Modern Mystic. An amusing distraction....many thanks.