The first point to make is that this is not the Great Depression that we are witnessing, though the downward trajectory of the world economy does mirror that event in many respects. The nature of the current economic crisis is, however, very different from the great depression. In particular, this crisis stems from an oversupply of labour in world markets. For regular readers, the following (taken from my recent Huliq article) will be familiar as one of the themes of the blog (and regular readers may therefore want to skip this passage):

I believe the logic of this point can not be denied, and I am still waiting for the mainstream to pick up on this. In the article, I go on to explain why this underlying cause led to the financial crisis. It was not lack of regulation, but rather it was the flood of money from the East into the West with insufficient investment opportunities to 'soak up' the money.The story of the economic crisis starts with the opening of China and India to world trade. Whilst both of these countries opened decades ago, it is only in about the last decade that their full impact has been felt on the world trading system. This appears to be a statement of the obvious, but the real implication is more dramatic than you might imagine; the opening of these countries has seen the world labour force roughly double in a period of about ten years.

It might be argued that the labour force has always been there, such that the doubling I propose is an exaggeration. However, in this context I have a very specific meaning for labour. I am referring to labour which is combined with technology, capital, and access to the world market. When seen this way, the increase in the labour supply represents an astounding increase in one of the key inputs into all economic activity.

This of itself might be a cause for the current crisis. For example, a massive expansion in supply would be expected to result in a decrease in the price of labour. As an analogy, imagine if the world supply/reserves of oil was to have doubled in ten years. Such a massive increase in the availability of one of the key inputs into economic activity might create revolutionary outcomes. Oil prices would be slashed, the petro economies would be in trouble, and there might be a deflationary surge and so forth.

However, it is only when we consider the relative supply of one of the inputs against the other inputs that the real reason for the economic crisis becomes apparent.

It is here that we have the real roots of the economic crisis, and where it is apparent that the emergence of countries such as China and India has created a zero sum gain. In particular, the point was reached some time ago where each gain in the economies of India and China means a relative loss in the economies of the traditionally wealthy countries. How has this situation arisen?

I have already identified that the world labour force has roughly doubled in the last ten years. At the same time, there has not been the doubling of the other inputs into the world economy. In crude terms, what this means is that the amount of inputs available to each worker to undertake economic activity has been reduced per capita.

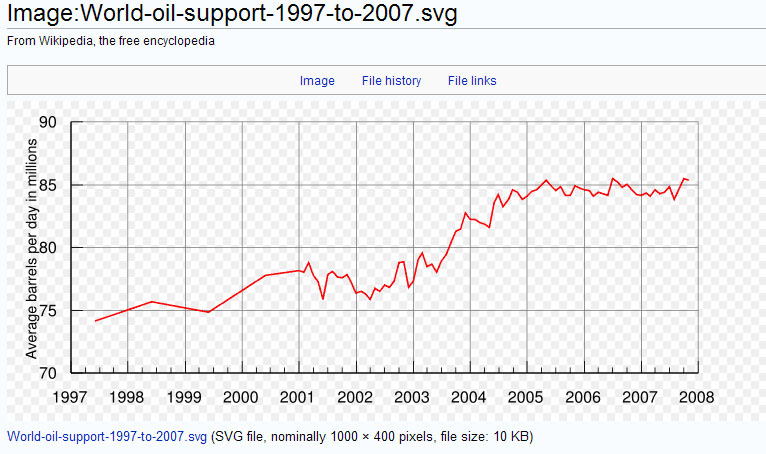

If we take the example of oil, in 1997 output was around 75 million bpd, and output had only climbed to about 85 million bpd in 2007 (a chart here shows the output - not a good source but the chart is usefully clear and conforms to charts from better sources). What we can see from 1997-2007 is an approximate doubling of the labour force, and only a tiny increase in the output of another key component of economic activity.

This quite literally means that the availability of oil per worker has seen a significant decline. In such a situation, there must be a consequence. If a worker in country A increases their utilisation of oil, then a worker in country B will have less oil available.

With regards to other commodities, it might be argued that the output has risen to meet the new demand from the expanded labour force. For example, copper has seen high growth in output from around 11 million tons to 16 million tons, and iron ore output nearly doubled. The problem with such expansion is that it is growth in a period of rapid development of the emerging economies, in which the demands on resources are particularly high. Think of the massive expansion of highways, tower blocks, apartments, airports and factories in China, and it is apparent where such increases might be absorbed.

{kind=link}

Instead of accepting that the world has changed, many analysts insist that a bit of tinkering here and there on regulation might have somehow saved us from the crisis (this has been reflected in recent comments). However, without closing borders, tariff protection, and capital controls, nothing was going to prevent the surge of money into the West from the East. Put bluntly, when any banker is handed large sums of money, they will take it and use it - they will not refuse it due to lack of good investment opportunities. The regulatory environment only had a role in shaping the nature of the inevitable bubble that would form under such circumstances.

Regulation and the financial system has been the focus of the economic crisis, with many referring to the economic crisis as a 'financial crisis', or the 'credit crunch'. Very few analysts and economists are looking at the underlying causes of the crisis, but are instead looking at the symptoms. I think that, in part, this is because the underlying reality is so difficult to accept, and in part because the problem is beyond any simple solutions. I have read the many solutions that are proposed, and they all have in common that they ignore the one single thing that really matters; the competitive position of the West in relation to the East.

For example, Krugman writes in his latest column that all can be saved, if the US government would just increase the stimuli into the economy. My response to such arguments are questions; How can this improve the competitive position of the US? Is it going to make a US textile worker more competitive? Is it going to make a toy factory more competitive? Is it going to make a furniture factory more competitive?

In other words, this does nothing to address the underlying problems. The US and Western economies are less and less able to compete.

In proposing this, he is merely proposing to add to an already unsustainable mountain of debt. Even CNBC 'gets it', and understands that the borrowing is exploding out of control and is unsustainable. They have lifted an AP article in which the level of deficits is as follows:

The country first got into debt to help pay for the Revolutionary War. Growing ever since, the debt stands today at a staggering $11.4 trillion — equivalent to about $37,000 for each and every American.People like Krugman wish to add to this. This is insane. The figure is per head, not per worker. Included in this figure are the retired and children. Furthermore, the numbers of retired are about to explode as the baby boomer generation starts retiring, and the cost will be huge (source the Economist).

Again from the CNBC article we have the following:

The Peter G. Peterson Foundation, established by a former commerce secretary and investment banker, argues that the $11.4 trillion debt figures does not take into account roughly $45 trillion in unlisted liabilities and unfunded retirement and health care commitments.In other words, at exactly the time that the Western world is being confronted with new and highly effective competition, the Western economies will need to support a massive fiscal expansion due to an ageing workforce. At exactly the time when the West needs to be saving money for this oncoming fiscal demand, the West is borrowing itself into oblivion. When we see the figures of debt per head in the US, there are going to be ever fewer workers to support that debt. According to the article in CNBC, the 'Interest payments on the debt alone cost $452 billion last year — the largest federal spending category after Medicare-Medicaid, Social Security and defense.'

The important point to note here is this is the figure for last year. The level of debt is rising and, if confidence in the US economy wanes, the cost of servicing this debt will also grow further, as lenders demand higher risk premia.

The most absurd part of all of this is that the economists and governments still measure this massive debt as a percentage of GDP. However, when they measure GDP it includes all of the activity from borrowing. This is a bit like a person measuring their income as their salary and their borrowing. The fact that their borrowing makes them appear more wealthy for the moment bears no relation to their actual income. If I earn £50,000 a year and borrow £10,000 a year I may appear to have an income of £60,000 but nothing will alter the reality that I only earn the £50,000 when I stop borrowing and start paying down the debt. When I start to pay back, rather than borrow, the illusionary wealth I counted in my income will be painfully apparent. I will be poor.

Within all of this debt accumulation and stimuli, the one thing that is missing is any attempt to address the fundamental problem of how the West might continue to compete with countries like China, India and Brazil. Tinkering with bank regulation is simply shutting the stable door after the horse has bolted. Borrowing more is simply digging the deficit hole deeper.

At the root of all of this frenzied activity to 'save' the economies of the West is an outright denial of reality. It is the point that I have made time and time again. How exactly are we going to pay back the debt?

The economies of the West are contracting. There is no plan for how exactly the challenge of places like China might be met. Even as I write, even as more borrowed money is poured into Western economies, the economy relentlessly shrinks, whilst government spending relentlessly rises. With each new tranche of borrowed money that appears in the economy, the potential for competitiveness in the future recedes. The cost of all of that borrowing is that the servicing of that debt must be supported at some point with ever more taxation.

It is like General Motors.

Even during the good times, they were borrowing money, and trying to support the salary, the pensions and health insurance of ever more workers. The trouble is that, the more they borrowed, the greater their costs as the debt mounted. The cost of all the benefits and entitlements, and servicing the debt mountain, was that there was less money for investment in plant and R&D, less money for all of the productive investments that might have kept the company alive. When the management confronted the workers and unions with the fact that the Japanese manufacturers in other states were costing so much less, the response was a refusal to accept the reality of the unsustainability of the position. The management caved in and, instead of addressing their cost base, they simply kept borrowing - until they reached a point of no return.

The difference between the Western governments and the GM management is that the Western governments are not even starting to confront us with the reality. Instead, they are doing the same thing as GM, and continuing to hand out entitlements that can not be afforded - and at the cost of ever growing debt. Another difference is that, in the case of countries, it is not entirely clear who might bail them out when they finally sink.

I think that this is the reason why the underlying cause of the economic crisis is being avoided. It means that we, in the West, must accept what the GM workers would not accept. We are simply uncompetitive. If we carry on as we do, then it can only end in disaster. It is not a pleasant reality to confront. Just as the GM workers refused to heed the reality of the situation, we collectively reject the reality of the situation.

Instead of accepting the reality, like spoilt children, we bleat about our entitlements. At the heart of it all is that we think that we are entitled to our wealth. It has still not entered our complacent minds that, as long as a Chinese or Indian worker is willing to work for half our wage, we are too expensive. Instead we blather on about sweat shops, when most Chinese workers are simply grateful to be given freedom from the grinding life as a peasant on the land. As I once argued with an individual, are you willing to stand outside a Chinese village and turn back the peasants who seek a better life in the cities?

This is the reality. The people in emerging economies want to get richer, and have a life like ours. As time passes by, they are going to take a greater share of the wealth in the world. They are hungry for success and willing to compete with us.

The real question that is not being raised is this; are we willing to compete with them?

All of the actions of government to date mirror the actions of GM. The entitlements continue, the cost base is growing as ever more workers retire. The numbers of retired in need of support grow such that each worker must shoulder a greater burden of retirement costs. The borrowing to support the benefits grows, the cost of servicing the debt grows, even as output and competitiveness declines in a slow death spiral.

How bluntly can I put this?

We are in a competition. We are losing.

To use the metaphor of a marathon race, we seem to believe that we can win the race by putting more fat on our bodies. The fact that this means that we have more weight to carry eludes us. The more that we fall behind in the race, the more we eat...and the more weight we have to carry through the rest of the race.

It is time to grow up and face reality.

Note 1:

I have some quotes from some very early posts which are perhaps appropriate to this article. Many refer to the UK in particular, but apply more broadly to what we have seen, for example, in the US. The point is that, since I wrote these posts, the situation has simply become worse, not better. As the crisis emerged, the underlying reality was apparent. We are not facing the competition, we are refusing to restructure, and refusing to accept that the world has changed. I present the quotes as a progression of frustration:

November, 2007: An economy built on bubbles...

The UK has been seen as a stable and expanding economy, an economic success, and this belief has attracted the inflows of money available for lending. The problem here is that it is the inflow of cheap money that has supported debt accumulation by consumers, and this in turn has made the economy appear so successful.'November, 2007: The illusions of economists....

I am sitting in China as I write this, and I feel a sense of regret. For the last few years I have had a deep foreboding about the UK economy. In particular my mind has continually returned to the question of ‘where’s the beef’, by which I mean where is the real earning, the real source of wealth in the UK economy. However hard I have looked, I have failed to see it, and now I suspect that the myth of the economic success of the UK economy is about to be exposed. My sense of regret is that I did not write this earlier. The majority of mainstream economists have remained convinced that some kind of economic miracle has been taking place in the UK. Miracle is a carefully chosen word, as it best describes the fact that only a miracle could allow the growth of the UK economy to be sustainable.November, 2007: How bad it will get....

The situation overall will be a massive contraction in the UK economy, a contraction that will see the UK step back in time in terms of economic development. The contraction will need to be deep and severe enough to reverse the illusory gains of the previous ten years (or even longer), and will require that the UK restructures its economy from top to bottom. It will, in effect, be the most significant crisis to hit the UK since the World War II. The only way out of the crisis will be to alter the fundamentals of the UK economy back to producing more goods and services for export led growth, and away from debt based growth in services. It will be a long, and very painful adjustment that will see the UK lose its place as one of the worlds’ leading economies, and recovery from the crisis will take many years.June 2008: Refusal to face reality and the delusion of the right to wealth....

Even as I have witnessed all of my predictions being correct, I have felt like a dismayed onlooker watching the progress of a car crash. Whilst my rational mind is observing, my emotional self simply can not grasp what is happening. Basically, like everyone else, it is very hard for me to accept that the severity of this economic crash can be as dramatic as it will actually be. Whilst reason says that this is going to be a disaster, the underlying belief that the UK economy can't just collapse still persists. After all, the UK has had crises before, and always returned to wealth and growth. Surely it must?July 2008: The dilemma that is not being confronted....

I read a very interesting example of this kind of thinking when I was reading some philosophy of science (sorry, I forget where I read it). The example given was a chicken that woke up every morning, and every morning the farmer fed the chicken. As a result the chicken believed that the farmer was a good thing - right up to the point where he chopped off the chicken's head. In the same way we have come to believe that the UK has some right to have the status of being a wealthy and successful economy. It always has been in the past, so why not now? The truth is that a successful economy is not a 'right', but something that has to be earned.

The trouble with the UK is that we expect wealth as a 'right'. It is this same thinking that has infected my thinking, and stopped me from considering the depth and severity of what is now occurring in the UK economy. In my essay, I suggested that the gains in GDP over the last 10 years will be lost, as the UK economy shrinks. However, I now think it will be far worse than this.

In particular, the problems with credit and the banks are going to reach their real crisis in about six to eight months time. The reason is that the fallout of the sub-prime fiasco is just the start. The next phase will be the consumer credit crisis and the SME crisis - and the results will be equally as dramatic, but with the added pain of hitting the banks when they are already suffering severely.

So what are these crises. The first is that consumer credit was already reaching breaking point, where many households were borrowing to repay borrowing. This was, in any event, unsustainable. Added to this factor, the story of inflation needs no more retelling. Finally, we have the spectre of rapid increases in unemployment, and it will be this development that will spark the second banking crisis. In particular the number of delinquent loans will start rising rapidly as unemployment increases, and accelerating concerns about the already weak balance sheets of the banks will see even greater tightening of credit conditions. Furthermore, unemployment will see even more mortgage defaults, and the banks will be trying to sell assets into a falling market. Quite simply, their losses are going to be staggering.

The second problem will come from the Small / Medium size businesses. As the economy turns down, think of the small traders - such as restaurants, who are already only marginally profitable. These will rapidly fail, in many cases leading to losses for the banks. Even the medium size companies, with a better financial base, are going to be negatively effected by the consumer downturn, and their failures will hurt the banks even more.

Remember that these problems are going to hit the balance sheets of banks when they are already tattered, and hit the reputation of the banks when their reputations are at a low.

This, in some senses, is stating the obvious. However, what is not obvious (apparently) are the points made in my essay about the money-go-round that has been the base of the UK economy. It is the lack of any fundamental strengths in the UK economy that will make the difference. It is like the game of 'Kerplunk' where, when you pull out enough straws, the balls come crashing down. Right now, the straws are being pulled.

So what now? I guess, wait and see. The only thing I think I would suggest is to make sure that any savings that you have are not in one bank, or one organisation. There are likely to be a quite a few bank failures, with the risk in about 6 months time. If the disaster has not happened in a year, then we can start smiling again. [we do not appear to be smiling now]

Taxation as a percentage of GDP has risen, and will need to rise further as tax revenues decline with recession, and expenditure increases (e.g. from paying benefits - increase in unemployment). Alternatively the government will need to cut services, thereby further increasing unemployment. In fact, whatever the government does, there is no solution, as increasing tax will further hurt the economy, or cutting services will increase unemployment. In short, increase tax/decrease tax - both will have the short term effect of plunging the economy deeper into recession. For the long term, cutting services is the only answer, but will Gordon Brown have the courage to make that decision? It is also worth noting that, whilst many other countries have been cutting taxation, Gordon Brown increased taxation. The expansion in the UK of the state and increased taxes have created a structural problem in the economy, and there is no way to unwind the problem without severe pain.July 2008: Confronting the competition....

However, having said all of this, I am not sure that we can take all of this for granted any more. As I have already suggested, the world has changed and is still changing. The rising power of the East is a fact of life, and the impact of that rise is only now becoming apparent. It is for this reason that I argue against the complacency that seems so prevalent. Just repeating that 'it will all be OK' will not make it so.July 2008: It is not the credit crunch, it is the lack of competitiveness....

As it is, I am relieved that finally the severity of the situation is starting to sink in. My ongoing worry is that the economists will start to blame the 'Credit Crunch' (an animistic beastie that serves as an explanation for all woes), rather than face the reality that the structures of the Western economies are now unsupportable. Until they grasp this idea, I worry that policy will carry on down the same road that has already led to this economic dead end.July 2008: The competition explained.....

However, I remain optimistic that the economists may (when confronted with the raw reality) manage to untangle themselves from their charts and discredited theory to actually think about the situation and how it has arisen. One of the first signs is the re-emergence of monetarism, though that of itself will only provide a small part of the answer. Click here for an example of the monetarist debate in the Telegraph.

If I was to summarise the root of the problems that we are seeing, I would have to refer you to my post on the 'Cigarette Lighter Problem'. At some point I hope to expand on this article, as I am still not sure that readers are grasping the magnitude of the problem that it represents (as it is an article that has received no comments).

In the meantime, reach for your hard hats, as the ride is about to get bumpy. As I have said before, the next shock will come in about 6 months when the second tranche of bad loans hit the balance sheets of the banks. As the economy turns down, unemployment goes up, a large amount of the credit that has been dished out irresponsibly will go bad. There will be at least a few bank failures, so spread your risk across institutions.

For the moment I will focus on China, as that is the country I know most about.(this last post is not very well written, but I hope the message is clear)

In the case of China, it opened to the West following the reforms of Deng Xiaoping and, from a modest start, saw an accelerating pace of growth, albeit starting from a low base. The momentum of that growth only started to be felt in the late 90s. At that time, for consumer goods, the whole Chinese economy (if I remember correctly it was a person from Nestle who I spoke with) was of similar size for consumer goods as Germany. Although there had been excitement about China before this, it was only at this point that everybody started to take notice, and that the pace of growth really represented a major shift in the world economy.

So what was happening when China opened up. The extraordinary thing that occurred was actually the conjunction of two vitally important processes. The first of these was the introduction of a massive source of labour into the world market, in this case nearly a billion new units of labour (and no, they were not all poorly educated, as even in the late 90s China was churning out large numbers of university graduates). Now this, of itself, was not important. There had always been large sources of cheap and untapped labour around the world, but most of the labour remained under utilised. What made the real difference with China, was the massive investment and technology transfers that were taking place from West to East.

China emerged onto the world market with a government that was uniquely business oriented (at least by the 90s), with their legitimacy built upon the foundations of ongoing economic growth. To facilitate such growth they built infrastructure, and a framework that told the Western businesses that it was a safe bet to invest in China for the long term. The result was a flood of foreign direct investment, and a flood of technology and know-how into China.

It is at this point we come to something rather special about China, and that is Chinese culture. The miracle in China was that Mao ever managed to pull off the communist revolution. I will not to into history here (even though I have a passion for modern Chinese history), to explain how it happened. The important point I would like to make is that there is something in Chinese culture which seems to make them (in general) naturally good businesspeople. If you visit Vietnam, Malaysia, Indonesia and so forth, you will find Chinese businesspeople at the top of the economy, despite their being minorities.

So what does this conjunction of factors add up to? The first point to make is that, in order for a massive supply of labour to be brought into a market, it takes more than just existence. In order for the labour to come into play, it requires the technology, capital, infrastructure and will. In the case of China, all of these elements came into play.

The result is that China had actually managed to bring a huge amount of labour effectively into the world market,. That process is still continuing, and still has substantial reserves still waiting to come into the market. This labour includes every level of skill and education.

Basic economics says that if supply increases, then prices will come down. We then have to ask what will happen when such a large pool of labour enters the world market? Will the price of labour go down? Well, of course it will........it is basic economics. What has made the real difference here is that the entry of this labour has been supported by an equalisation of capital and technology. All the Chinese had to do was learn how to do business, something for which they seem to have a cultural talent for. This has also occurred over the last twenty years.

Now if we accept this, how does this explain the current state of the world economy? The first thing to note is the balance of payments deficits of the West have been supported by capital accumulation in the East. This has seen a massive transfer of wealth from West to East. The East has continued to lend to the West on the basis that, like the West itself, it believed that the West was naturally more stable and a solid economic bet (sorry for the metonymy here, but it simplifies the expression of the ideas). As such the West has been going steadily further into debt, with both consumers and government borrowing like madmen. All the time both the lenders and borrowers were under the illusion that this situation was sustainable.

The result of all of this spending was an illusion in the Western world that nothing had changed. We had moved into the post-industrial service based economy. The share of manufacturing in the economy steadily declined and the economists all accepted this as a perfectly sustainable new economic order. The reality was that massive borrowing was just delaying the inevitable, the readjustment of the world economy to the massive input of productive labour. In delaying the impact of this adjustment, the imbalances have actually become far greater than they would otherwise have been. Even now, the West is still not prepared to take on the new competition of the emerging economies, in particular China. If anything, the West is in a far more grave situation than would have otherwise been the case. The massive debt that has been accumulated must now be repaid, and this at a time when the West desperately needs capital to invest in rebuilding collapsing economies.

[and]

Furthermore, it will become apparent that many of the things that we have taken for granted in the West will become unaffordable, such as bloated government and welfare states. Quite simply, if we are to compete with the East, we must either be adding significantly more value than the East can manage, or we need to have at least a comparable cost structure. The latter option looks more realistic.

As I have said, this is a very quick review and is short on facts and figures. However, the principles are very clear, and I believe rational. The current crisis is therefore a rebalancing of the world economy and, unless the West responds to the reality, the problems will persist, if not get worse. We have had very little competition and took 'top dog' status as a natural course of affairs.

We are now learning that this is just not the case.

I could continue with ever more sections from previous posts. As time has gone on, the one thing that is unchanging is the refusal to accept the reality that we are being confronted with. As each stage of the economic crisis progresses, the focus is on anything but the underlying reality. This is not a financial crisis, but an economic crisis.

With each prediction from governments and economists that recovery is around the corner, more problems appear. The current talk of 'green shoots' is already fading. Why - because nothing has yet been done to address the underlying problems.

Note 2: I do not have time to address all of the comments from the last post, but have managed some replies in the comments section. All comments are appreciated, as are the links to various articles. The latter are often very useful leads for me, so thanks.

Note 3: This from the Times today:

It seems that at least the civil service is starting to deal with reality. The trouble is that the collective 'we' that are the public, and the politicians, are simply not ready for this.Secret “doomsday” plans for 20% cuts in public spending are being prepared by senior civil servants, who fear politicians are failing to confront the scale of the budget black hole.

Whitehall mandarins have begun creating detailed dossiers containing reductions in expenditure that are far deeper than the more modest savings being proposed by Labour and Conservative politicians.

[and]

Senior civil servants have let it be known that they are sceptical about the claims made by both main parties on public spending.

While Labour wants to increase expenditure despite the £175 billion budget deficit, the Tories, using figures from the Institute for Fiscal Studies (IFS), have acknowledged the need for cuts of up to 10%.

Mandarins, fearing a prolonged recession and a collapse in tax revenue, have begun planning for more severe cuts of up to 20%.

The dossiers will be handed to cabinet ministers the day after the next general election, whichever party wins.

Jonathan Baume, general secretary of the FDA, which represents senior civil servants, said: “It could be even worse for some departments than the IFS has predicted.”

Lord Turnbull, the former cabinet secretary, echoed the warning. “The civil servants will have to assume that whatever both parties are saying today, in the end they will have to be bolder. What politicians say on the record will underestimate the magnitude of the task,” he said.